epal’s Banking Sector Shows Strong Capital Base as of Mid-June 2025

Author

Nepse Trading

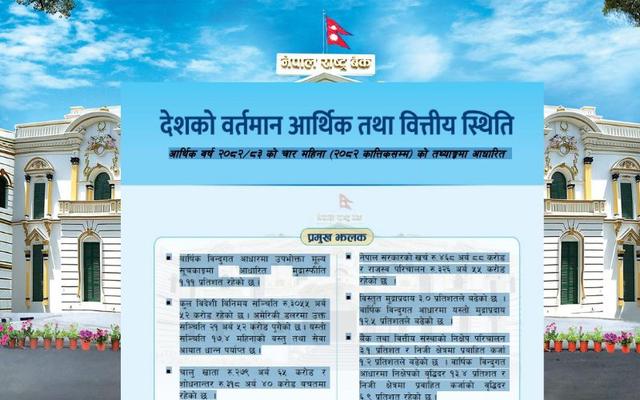

As per the latest financial indicators published for the period ending Jeth, 2082 (mid-June 2025), Nepal’s banking sector continues to exhibit a stable capital base, ensuring resilience against potential financial shocks. The capital adequacy ratios, a critical metric used to assess the capital strength of financial institutions, remain well above regulatory thresholds across all classes of banks.

Class “A” commercial banks have reported a Core Capital to Risk-Weighted Assets (RWA) ratio of 9.50%, while Class “B” development banks and Class “C” finance companies posted 10.27% and 10.55% respectively. The overall average for the banking sector stood at 9.58%, indicating a healthy buffer of core capital. This core capital—comprising primarily of equity and disclosed reserves—is vital for absorbing unexpected losses and maintaining market confidence.

Looking at the Total Capital to RWA ratio, which includes both core and supplementary capital, Class “A” institutions reported 12.34%, Class “B” reported 12.97%, and Class “C” stood at 12.51%. The aggregate sector-wide total capital ratio averaged 12.40%, comfortably above the minimum regulatory requirement set by Nepal Rastra Bank.

These figures highlight that all categories of financial institutions are maintaining strong capital positions, which is crucial for sustaining credit growth while also safeguarding against systemic risks. With consistent capitalization levels, Nepal’s financial system appears well-positioned to support future economic expansion and meet international banking norms such as Basel III requirements.

In summary, the capital adequacy ratios signal a positive outlook for Nepal’s banking sector, underpinning financial stability and investor confidence as the country moves through fiscal year 2082/83.