By Dipesh Ghimire

CORBL Faces Financial Decline: Urgent Interventions Needed

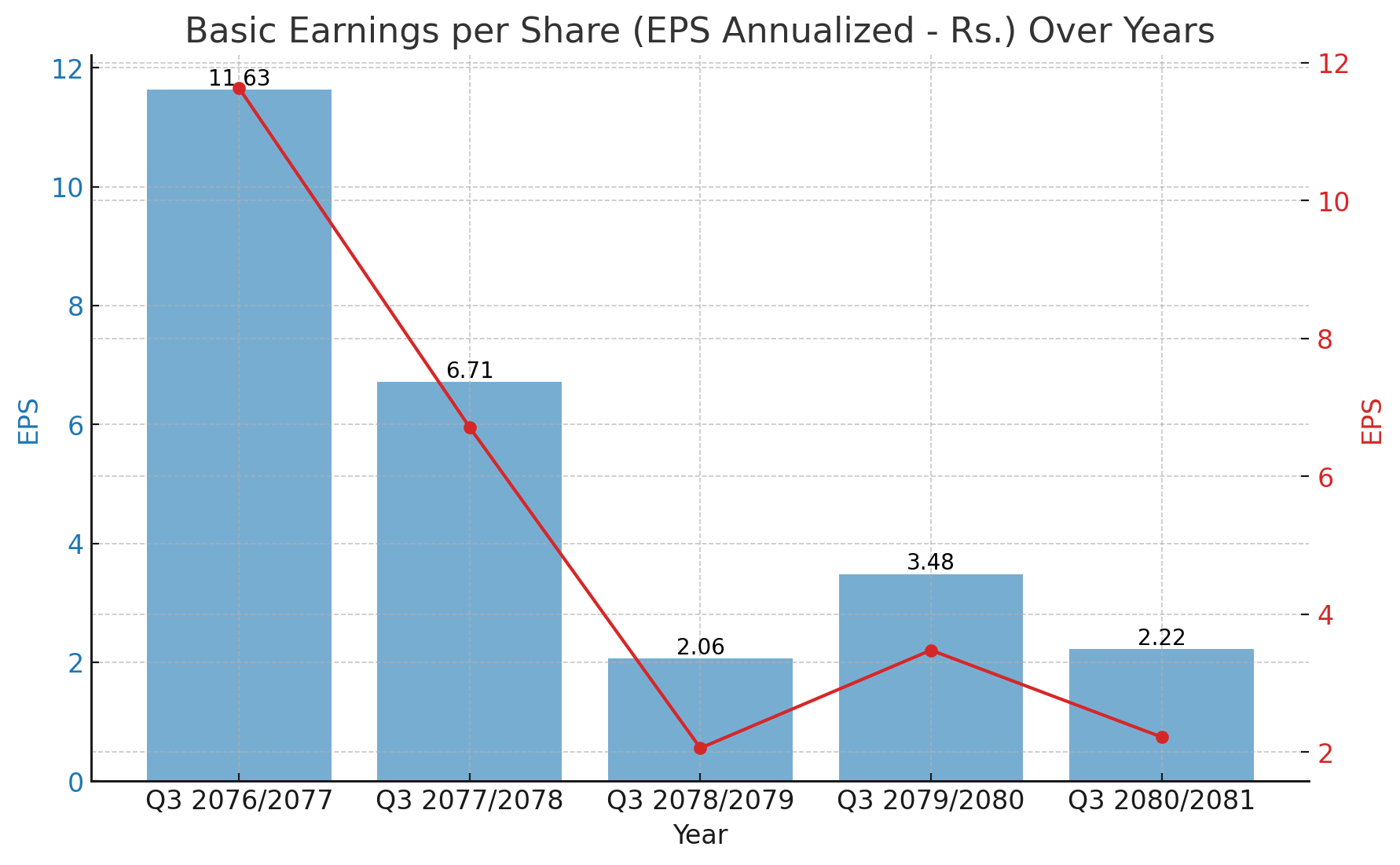

CORBL DEVBANK Shows Decline in EPS Over Five Years

CORBL DEVBANK's earnings report for the third quarter of 2080/2081 reveals a significant decline in its basic earnings per share (EPS) over the past five years. The data indicates a downward trend that could raise concerns among investors and stakeholders.

Detailed EPS Analysis:

Q3 2080/2081: The EPS for the most recent quarter stands at Rs. 2.22. This figure shows a slight decrease from the previous year's Q3 EPS of Rs. 3.48.

Q3 2079/2080: At Rs. 3.48, this year saw a modest recovery from the previous year's low but was still significantly lower than earlier years.

Q3 2078/2079: The EPS further dipped to Rs. 2.06, reflecting a continuing decline in profitability.

Q3 2077/2078: A notable drop occurred this year, with the EPS at Rs. 6.71, down from Rs. 11.63 the previous year.

Q3 2076/2077: The highest EPS recorded in this five-year span was Rs. 11.63, indicating much stronger financial performance compared to subsequent years.

Interpretation:

The consistent decline in EPS suggests several underlying issues that CORBL DEVBANK might be facing. The highest EPS of Rs. 11.63 in Q3 2076/2077 indicates that the bank was performing well at that time. However, the sharp decrease to Rs. 6.71 in the following year marked the beginning of a downward trend.

Several factors could be contributing to this decline:

Market Conditions: Changes in the economic environment, interest rates, and banking regulations could have adversely affected the bank's profitability.

Operational Challenges: Increased operational costs, inefficiencies, or strategic missteps might have led to reduced earnings.

Competitive Pressure: Heightened competition in the banking sector could have eroded the bank's market share and profitability.

Outlook:

Investors need to closely monitor CORBL DEVBANK's strategies to address these challenges. Efforts to improve operational efficiency, strategic initiatives to enhance market position, and adapting to changing market conditions will be crucial for reversing the downward EPS trend.

In summary, while CORBL DEVBANK has shown resilience by slightly improving its EPS in Q3 2079/2080, the overall trend remains concerning. Strategic interventions and market adaptability will be key to ensuring long-term financial health and regaining investor confidence.Rising Non-Performing Loans at CORBL DEVBANK: A Concern for Stakeholders

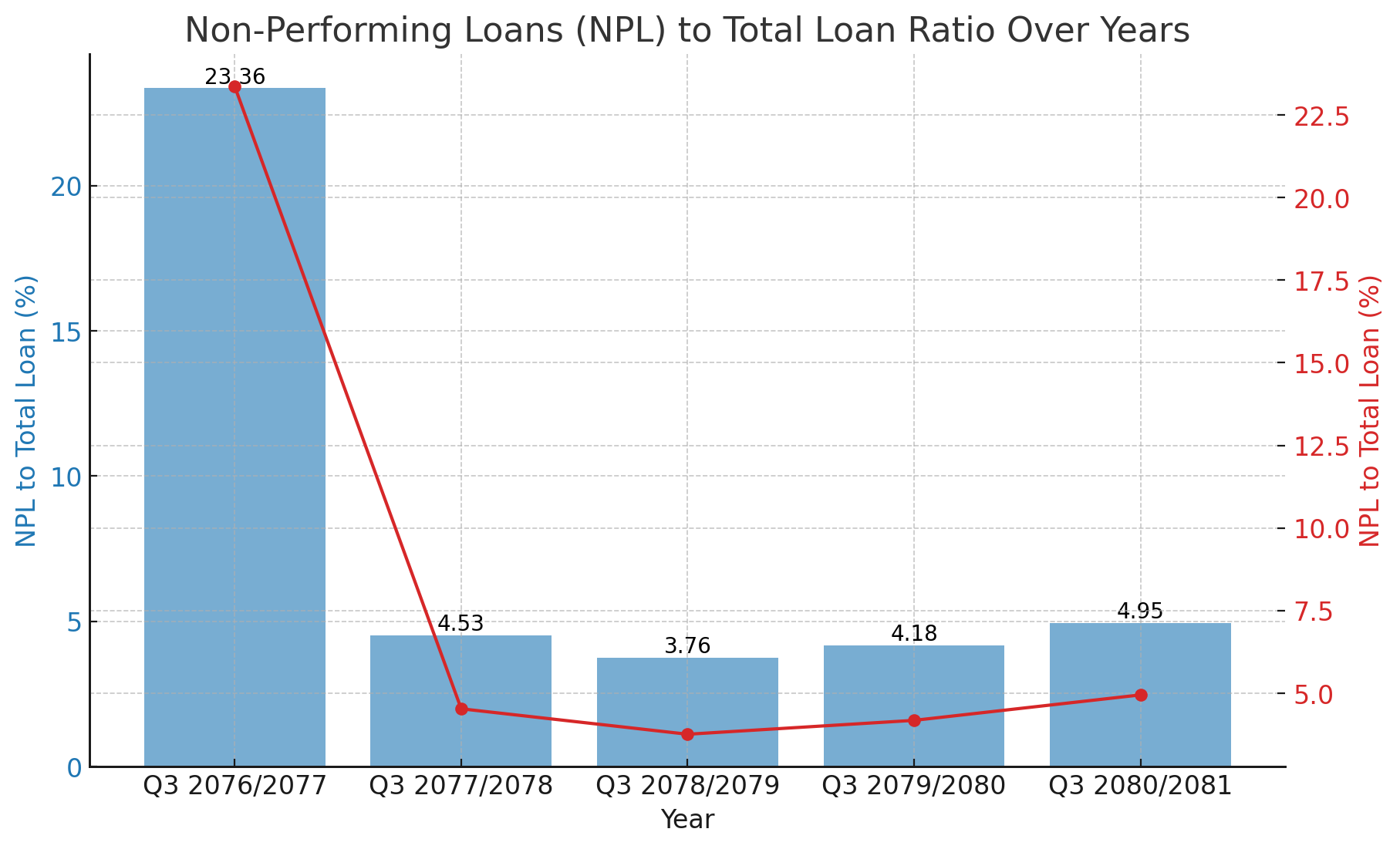

CORBL DEVBANK's latest financial report highlights an increase in its Non-Performing Loans (NPL) to Total Loan ratio over the past five years. The data suggests a troubling trend that may impact the bank's overall financial health and stability.

Detailed NPL Analysis:

- Q3 2080/2081: The NPL ratio for the most recent quarter stands at 4.95%. This marks an increase from the previous year's Q3 ratio of 4.18%.

- Q3 2079/2080: The NPL ratio was 4.18%, showing an upward trend from the previous year.

- Q3 2078/2079: The ratio stood at 3.76%, reflecting a concerning rise in non-performing loans.

- Q3 2077/2078: A slight increase in the NPL ratio to 4.53% was observed.

- Q3 2076/2077: The highest NPL ratio recorded in this five-year span was 23.36%, indicating significant challenges faced by the bank.

Interpretation:

The increasing NPL ratio is a red flag for CORBL DEVBANK. Non-performing loans are loans in default or close to being in default. A higher NPL ratio indicates that the bank is struggling with a higher proportion of bad loans, which can have several implications:

1. Financial Health: An increasing NPL ratio can adversely affect the bank's profitability, as more resources must be allocated for loan loss provisions.

2. Credit Risk Management: The rising ratio may reflect weaknesses in the bank's credit risk management practices, requiring a review and strengthening of loan approval and monitoring processes.

3. Investor Confidence: A higher NPL ratio can erode investor confidence, as it signals potential instability and risk in the bank's loan portfolio.

To address the rising NPL issue, CORBL DEVBANK needs to implement robust measures aimed at improving loan recovery and strengthening credit risk management practices. These measures could include stricter credit assessments, enhanced monitoring of loan performance, and effective recovery strategies for distressed assets.

In conclusion, while the EPS figures show a declining trend, the rising NPL ratio adds another layer of concern for CORBL DEVBANK. The bank's ability to manage and mitigate these risks will be crucial for ensuring long-term financial stability and maintaining stakeholder confidence.

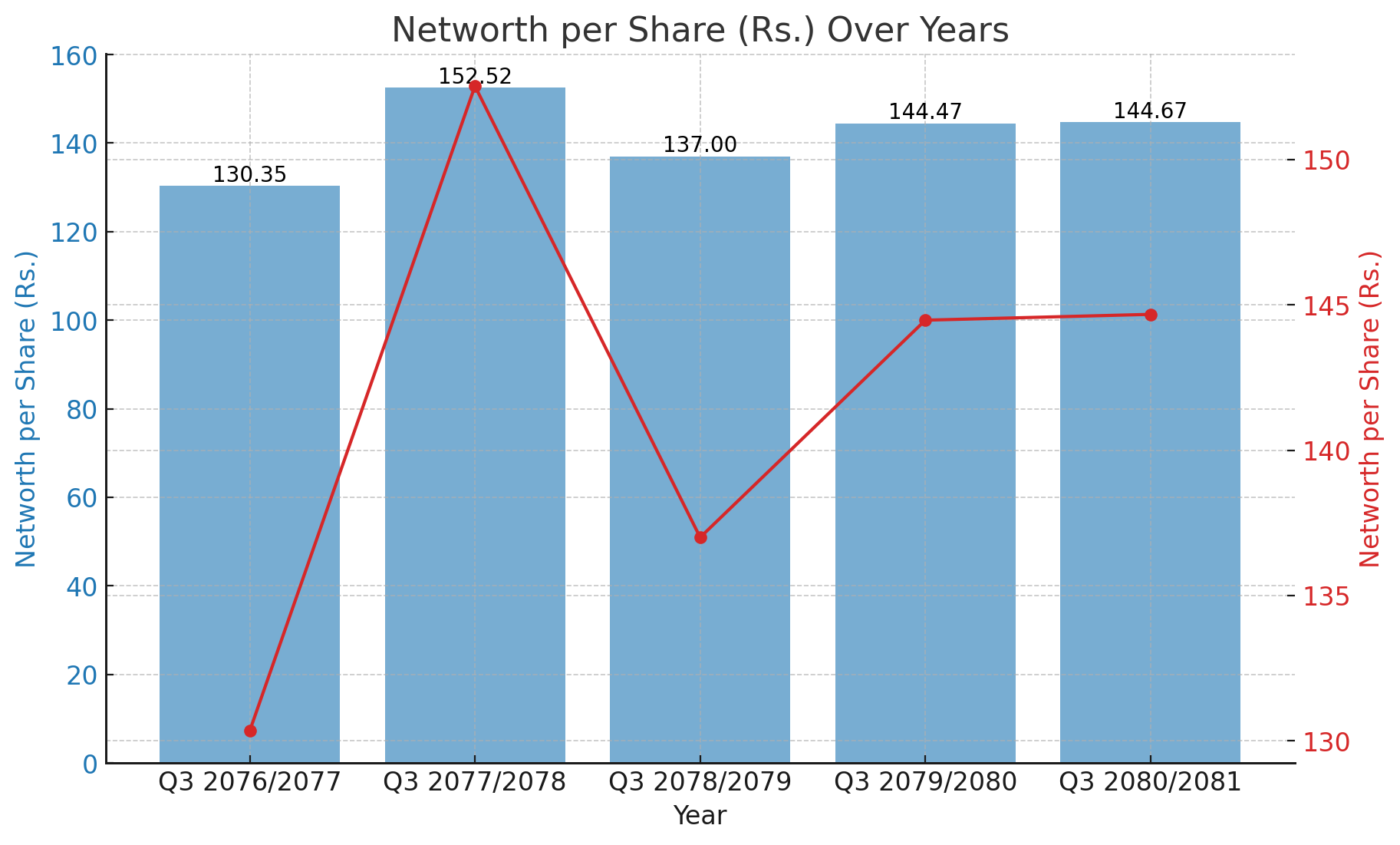

Stable Networth Per Share at CORBL DEVBANK Amidst Other Challenges

CORBL DEVBANK's financial data reveals a relatively stable trend in its net worth per share over the past five years. This stability contrasts with the declining EPS and increasing NPL ratios, suggesting that while profitability and loan quality are areas of concern, the bank's overall net worth has remained resilient.

Detailed Networth Per Share Analysis:

Q3 2080/2081: The net worth per share for the most recent quarter is Rs. 144.67, showing a slight increase from the previous year.

Q3 2079/2080: The net worth per share was Rs. 144.47, maintaining a stable level compared to the year before.

Q3 2078/2079: The figure stood at Rs. 137, indicating a steady growth in net worth.

Q3 2077/2078: The highest net worth per share during this period was Rs. 152.52, reflecting a strong financial position at that time.

Q3 2076/2077: The net worth per share was Rs. 130.35, marking the beginning of a period of growth.

Interpretation:

The stability in net worth per share indicates that CORBL DEVBANK has been able to maintain its asset base despite facing challenges in profitability and loan quality. This could be attributed to several factors:

Asset Management: Effective management of assets and liabilities has helped the bank sustain its net worth.

Capital Retention: Adequate capital retention policies and reinvestment of earnings have contributed to maintaining the net worth per share.

Resilience: The bank's ability to withstand external economic pressures and internal challenges reflects its underlying financial resilience.

Outlook:

While the stability in net worth per share is a positive sign, CORBL DEVBANK needs to address its declining EPS and rising NPL ratios to ensure long-term financial health. Strengthening profitability and improving loan quality will be essential to enhance overall financial performance.

In summary, CORBL DEVBANK's net worth per share has shown commendable stability over the past five years. However, the bank must focus on strategic initiatives to boost profitability and manage credit risks effectively. By doing so, it can ensure sustained growth and stability, benefiting its stakeholders and maintaining investor confidence.

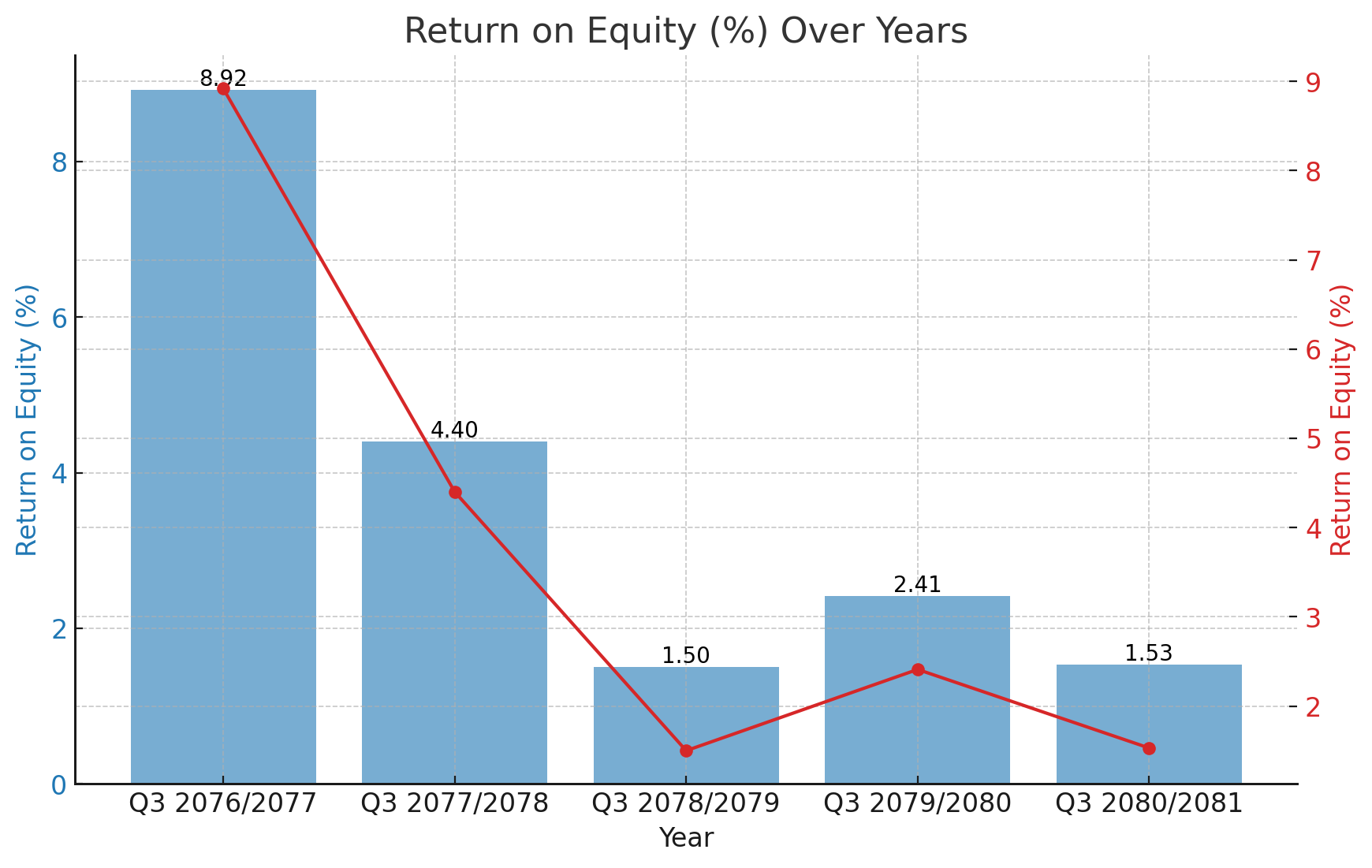

Declining Return on Equity at CORBL DEVBANK: A Challenge to Profitability

CORBL DEVBANK's financial data reveals a significant decline in its Return on Equity (ROE) over the past five years. ROE is a measure of a company's profitability relative to shareholders' equity, and a declining trend can be indicative of underlying issues in the bank's ability to generate profits.

Detailed ROE Analysis:

Q3 2080/2081: The ROE for the most recent quarter is 1.53%, marking a decrease from the previous year's ROE of 2.41%.

Q3 2079/2080: The ROE was 2.41%, which, while low, showed a slight improvement from the year before.

Q3 2078/2079: The ROE stood at 1.5%, reflecting continued challenges in profitability.

Q3 2077/2078: The ROE was 4.4%, a significant drop from earlier years but still better than recent figures.

Q3 2076/2077: The highest ROE in this period was 8.92%, indicating a much stronger ability to generate profits from shareholders' equity at that time.

Interpretation:

The declining ROE trend highlights several potential issues for CORBL DEVBANK:

Profitability Concerns: The consistent decrease in ROE suggests that the bank is struggling to generate sufficient returns from its equity base.

Operational Efficiency: Lower ROE may indicate inefficiencies in the bank's operations, requiring a review of cost management and revenue generation strategies.

Investor Confidence: A declining ROE can erode investor confidence, as it signals reduced effectiveness in utilizing shareholders' funds to generate profits.

Outlook:

To address the declining ROE, CORBL DEVBANK needs to focus on strategies that can enhance profitability and operational efficiency. This could include cost-cutting measures, optimizing revenue streams, and improving asset management practices.

In summary, CORBL DEVBANK's ROE has shown a concerning downward trend over the past five years. While the bank's net worth per share has remained relatively stable, the declining ROE underscores the need for strategic interventions to boost profitability and maintain investor confidence. By addressing these challenges, CORBL DEVBANK can work towards enhancing its financial performance and securing long-term growth.

Zero Distributable Profit Per Share at CORBL DEVBANK: A Concern for Shareholders

CORBL DEVBANK's financial data reveals that the bank has reported zero distributable profit per share over the past five years. Distributable profit per share is a crucial indicator for shareholders, as it reflects the portion of profit that can be distributed as dividends.

Detailed Analysis:

Q3 2080/2081: The distributable profit per share for the most recent quarter is zero, consistent with the previous years.

Q3 2079/2080: No distributable profit was reported, continuing the trend from earlier years.

Q3 2078/2079: The bank also reported zero distributable profit per share.

Q3 2077/2078: Similar to other years, no distributable profit was available for shareholders.

Q3 2076/2077: The bank reported zero distributable profit per share.

Interpretation:

The consistent lack of distributable profit per share over the past five years indicates significant challenges in generating sufficient profits to distribute to shareholders. This could be due to several factors:

Profitability Issues: The bank's overall profitability may be insufficient, leading to no surplus available for distribution.

Retained Earnings: The bank might be retaining all its earnings for reinvestment or to cover operational costs and losses.

Operational Challenges: Inefficiencies and high operational costs could be consuming the profits, leaving nothing for distribution.

Outlook:

For shareholders, the absence of distributable profits raises concerns about the bank's ability to provide returns on their investments. The bank needs to focus on enhancing profitability and operational efficiency to generate surplus profits that can be distributed as dividends.

In summary, CORBL DEVBANK's zero distributable profit per share over the past five years is a significant concern for shareholders. Addressing profitability and operational challenges will be crucial for the bank to ensure that it can provide returns to its shareholders in the future.