By Sandeep Chaudhary

NRB Concessional Loans Show Varied Trends Across Different Categories

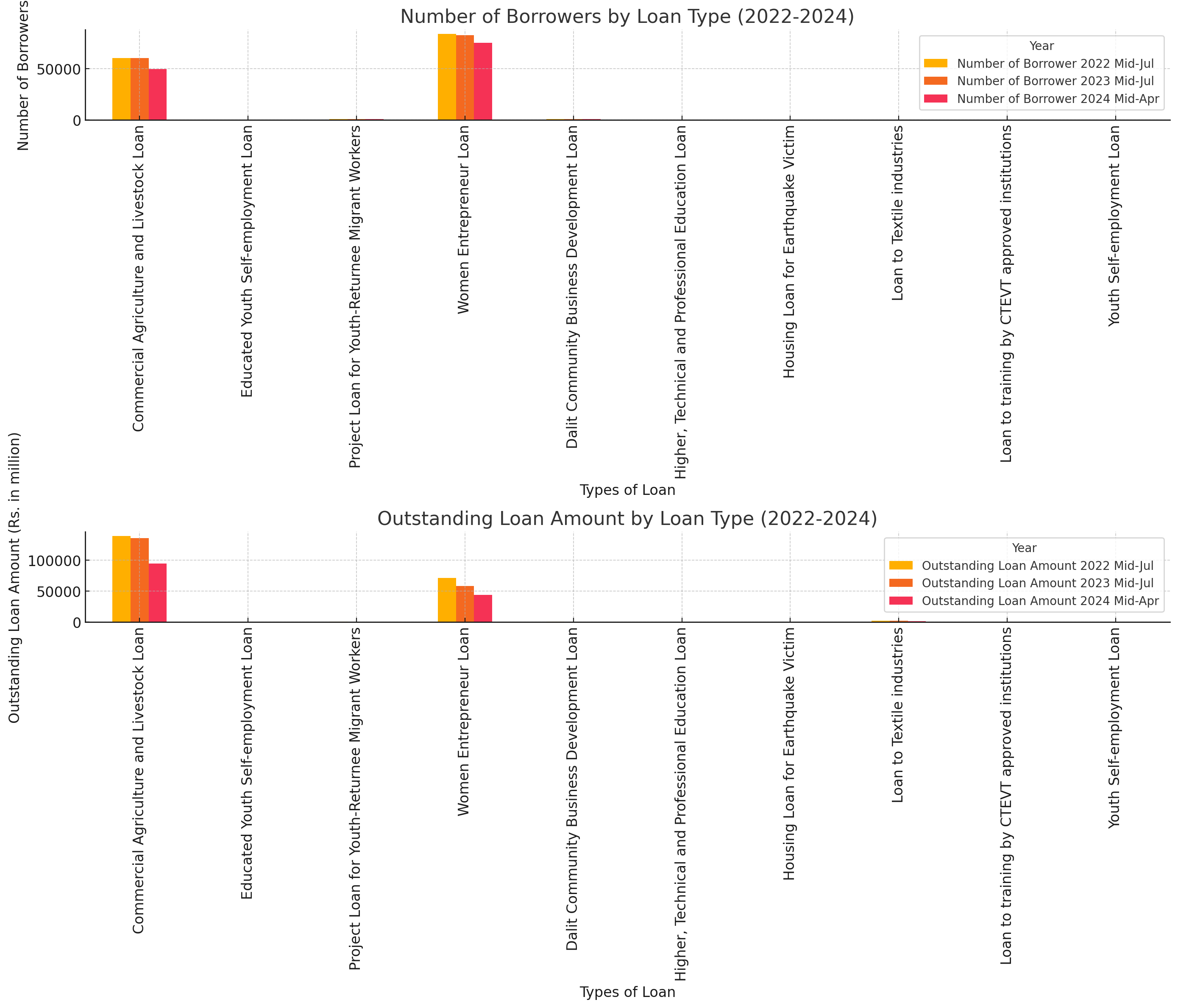

The latest data on concessional loans, as detailed in Table 46, highlights significant shifts in the number of borrowers and the outstanding loan amounts across various loan categories from 2022 to 2024. This report provides a comprehensive overview of these trends, offering insights into the economic activities and priorities of different borrower groups.

Commercial Agriculture and Livestock Loan: This category, primarily aimed at boosting agricultural productivity, has seen a notable decrease in the number of borrowers, from 60,545 in Mid-Jul 2022 to 49,648 in Mid-Apr 2024. Correspondingly, the outstanding loan amount has also reduced from Rs. 139,234.1 million in Mid-Jul 2022 to Rs. 94,849.3 million in Mid-Apr 2024. This decline suggests a potential shift in agricultural financing or a possible repayment of loans.

Educated Youth Self-employment Loan: The number of borrowers in this segment has shown a slight increase from 157 in Mid-Jul 2022 to 165 in Mid-Apr 2024. However, the outstanding loan amount has decreased from Rs. 76.1 million to Rs. 25.6 million, indicating a significant repayment or a reduction in loan size per borrower.

Project Loan for Youth-Returnee Migrant Workers: Loans in this category have witnessed a decrease in both the number of borrowers and the outstanding loan amount. The number of borrowers reduced from 952 in Mid-Jul 2022 to 795 in Mid-Apr 2024, while the outstanding loan amount decreased from Rs. 564.2 million to Rs. 294.6 million.

Women Entrepreneur Loan: There has been a significant increase in the number of women entrepreneurs availing loans, from 84,001 in Mid-Jul 2022 to 75,333 in Mid-Apr 2024. The outstanding loan amount, however, has decreased from Rs. 70,996.1 million to Rs. 43,794.6 million, reflecting either a trend of smaller loan amounts or effective loan repayment.

Dalit Community Business Development Loan: This category shows a slight decline in the number of borrowers from 1,097 in Mid-Jul 2022 to 982 in Mid-Apr 2024. The outstanding loan amount also saw a reduction from Rs. 582.3 million to Rs. 330.1 million, suggesting a decrease in loan uptake or successful repayments.

Higher, Technical and Professional Education Loan: The number of borrowers in this segment has remained relatively stable, with a slight increase from 148 in Mid-Jul 2022 to 165 in Mid-Apr 2024. The outstanding loan amount has seen a significant reduction from Rs. 36.3 million to Rs. 29.1 million, indicating effective loan repayments.

Housing Loan for Earthquake Victim: Borrowers in this category have decreased slightly from 208 in Mid-Jul 2022 to 179 in Mid-Apr 2024. The outstanding loan amount has also reduced from Rs. 38.9 million to Rs. 21.4 million.

Loan to Textile Industries: The number of borrowers in this sector remains low, and the outstanding loan amount has shown a decreasing trend from Rs. 2,358.5 million in Mid-Jul 2022 to Rs. 1,175.1 million in Mid-Apr 2024.

Loan to Training by CTEVT Approved Institutions: This category has a minimal number of borrowers and outstanding loan amounts, reflecting its niche target group.

Youth Self-employment Loan: Similar to other categories aimed at youth, this segment has maintained a consistent number of borrowers, with minor fluctuations. The outstanding loan amount has seen a slight decrease from Rs. 10.3 million to Rs. 8.5 million from Mid-Jul 2022 to Mid-Apr 2024.

Overall, the total number of borrowers across all loan categories has seen a decline from 147,393 in Mid-Jul 2022 to 127,212 in Mid-Apr 2024. The total outstanding loan amount has also decreased from Rs. 213,889.3 million to Rs. 140,496.5 million in the same period. This data suggests a broad trend of repayment and possibly stricter loan disbursement criteria or reduced demand for concessional loans.

These trends provide valuable insights for policymakers and financial institutions to understand borrower behavior and adjust their strategies accordingly to promote economic growth and financial inclusion.