Popular News

Hot

Stock

Top

dipesh

Trading

·By Writer Content

By Writer Content

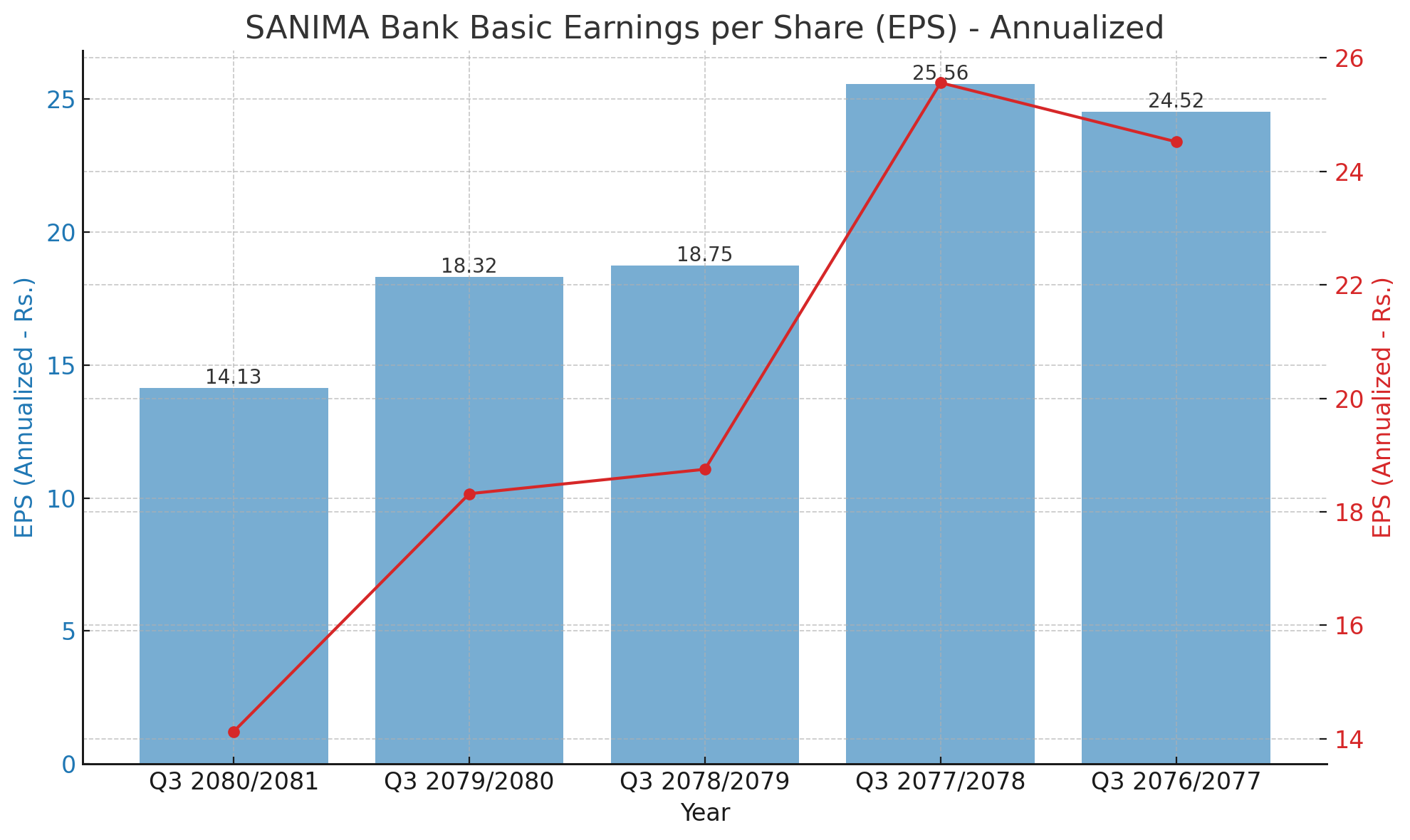

SANIMA Bank has released its financial report, revealing a noticeable trend in its Basic Earnings per Share (EPS) over the past five years. The data spans from the fiscal year Q3 2076/2077 to Q3 2080/2081, presenting both positive and negative shifts in the bank's financial performance.

Year-by-Year Breakdown

1. Q3 2076/2077: The EPS stood at Rs. 24.52. This year marked a high point for SANIMA Bank, demonstrating strong financial health and profitability.

2. Q3 2077/2078: The EPS reached its peak at Rs. 25.56. This increase reflects the bank's successful strategies and robust performance in that period, likely driven by effective management and favorable market conditions.

3. Q3 2078/2079: The EPS dropped slightly to Rs. 18.75. While still healthy, this decline may suggest initial signs of market challenges or internal shifts within the bank's operations.

4. Q3 2079/2080: A further decline to Rs. 18.32 was observed. This consistent decrease indicates ongoing issues, possibly related to external economic factors, increased competition, or regulatory changes impacting the banking sector.

5. Q3 2080/2081: The most recent report shows a significant drop to Rs. 14.13. This represents the lowest point in the five-year period, highlighting potential strategic missteps or adverse economic conditions that have considerably impacted the bank's profitability.

Interpretation and Future Outlook

The consistent decline in SANIMA Bank's EPS over the last three years raises concerns about the bank's ability to sustain its growth and profitability. Several factors could be contributing to this trend:

- Economic Environment: Fluctuations in the economic landscape, including inflation, changes in interest rates, and overall market volatility, could be affecting the bank's earnings.

- Competition: Increased competition from other banks and financial institutions might be eroding SANIMA Bank's market share and profit margins.

- Regulatory Changes: New regulations or changes in existing ones could be impacting the bank's operations and financial performance.

- Operational Efficiency: Internal factors such as cost management, investment strategies, and operational efficiency play a crucial role in financial outcomes. The decline suggests a need for SANIMA Bank to reassess its strategies and operations.

To address these challenges, SANIMA Bank may need to implement strategic initiatives focused on improving efficiency, exploring new revenue streams, and adapting to market changes. Strengthening customer relations and enhancing digital banking services could also provide a competitive edge.

In conclusion, while SANIMA Bank has faced a declining EPS trend, understanding and addressing the underlying factors can help the bank navigate through these challenges and aim for a rebound in the coming years. Investors and stakeholders will be keenly observing the bank's strategic responses and their effectiveness in reversing the current trend.

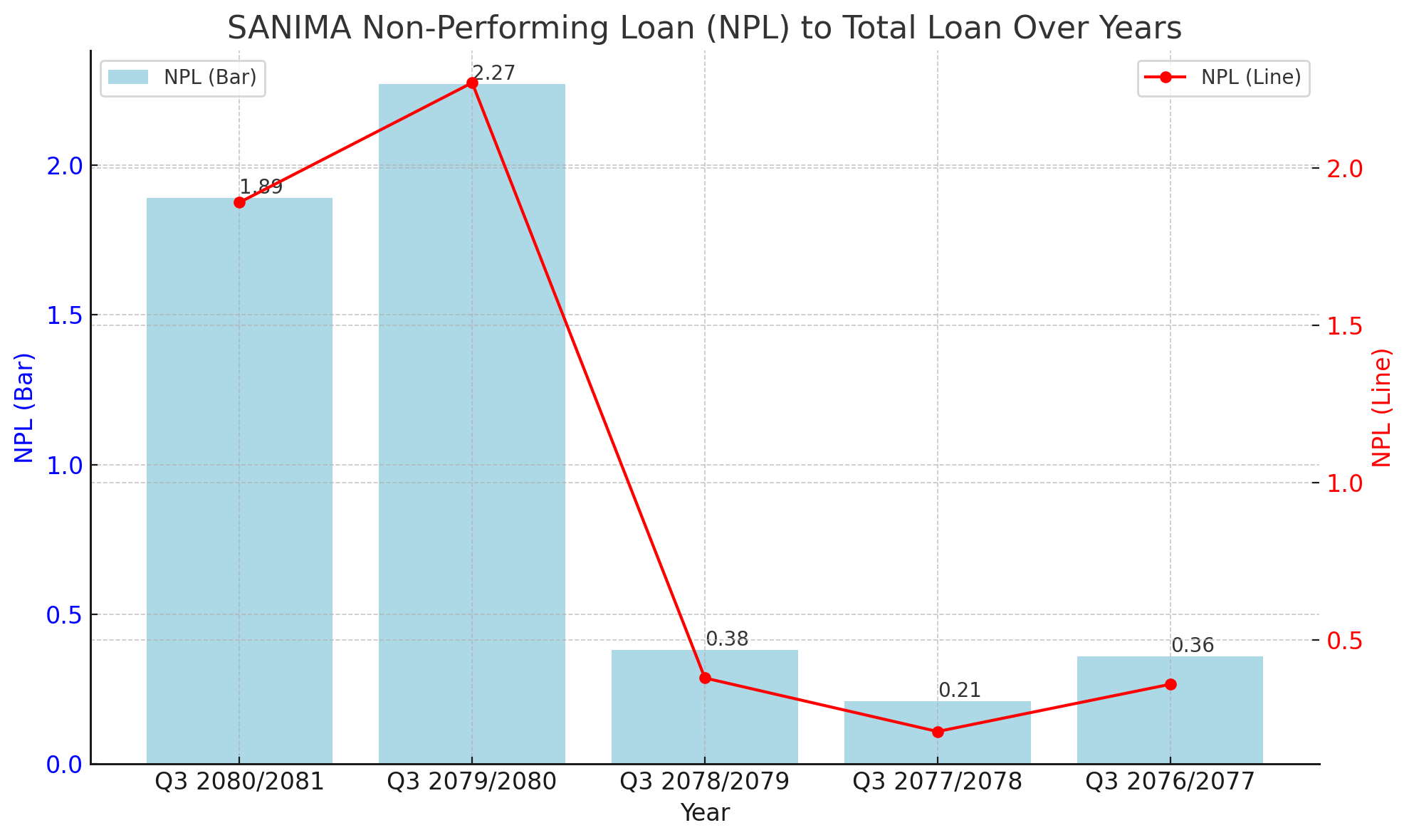

Over the past five years, SANIMA Bank has experienced fluctuations in its Non-Performing Loan (NPL) to Total Loan ratio, reflecting changes in loan performance and credit quality.

Q3 2076/2077: The NPL ratio was at 0.36%, indicating a relatively low level of non-performing loans compared to the total loan portfolio, suggesting effective credit management and strong loan performance.

Q3 2077/2078: A further reduction to 0.21% demonstrates exceptional loan performance and stringent credit control measures.

Q3 2078/2079: The NPL ratio slightly increased to 0.38%. This change, while minor, could indicate the beginning of emerging credit quality issues or external economic pressures affecting borrowers' repayment abilities.

Q3 2079/2080: A significant spike to 2.27% suggests a substantial deterioration in loan performance. This sharp increase could be attributed to adverse economic conditions, increased default rates, or internal challenges in credit risk management.

Q3 2080/2081: The ratio decreased to 1.89%, showing some improvement but still indicating elevated levels of non-performing loans compared to earlier years.

SANIMA Bank's Non-Performing Loans Show Signs of Stress Amid Economic Challenges

In its latest financial disclosure, SANIMA Bank reported notable changes in its Non-Performing Loan (NPL) to Total Loan ratio over the past five years. The data reveals both periods of strong loan performance and times of financial stress, painting a comprehensive picture of the bank's credit risk management and economic resilience.

In Q3 2076/2077, SANIMA Bank maintained a low NPL ratio of 0.36%, showcasing its effective credit management and solid loan portfolio. This positive trend continued into Q3 2077/2078, where the NPL ratio dropped further to an impressive 0.21%.

However, the subsequent year saw a slight uptick to 0.38%, indicating emerging challenges. The most significant change occurred in Q3 2079/2080, with the NPL ratio surging to 2.27%. This sharp increase points to substantial loan performance issues, likely driven by unfavorable economic conditions and rising default rates.

The most recent data for Q3 2080/2081 shows some recovery, with the NPL ratio declining to 1.89%. Despite this improvement, the elevated levels compared to earlier years suggest ongoing challenges in credit quality and loan performance.

The fluctuations in SANIMA Bank's NPL ratio highlight the bank's vulnerabilities to economic pressures and the importance of robust credit risk management strategies. As the bank navigates through these challenges, stakeholders and investors will be closely monitoring its efforts to stabilize and improve loan performance in the coming years.

By understanding and addressing these underlying issues, SANIMA Bank aims to strengthen its financial health and enhance its resilience against future economic uncertainties.

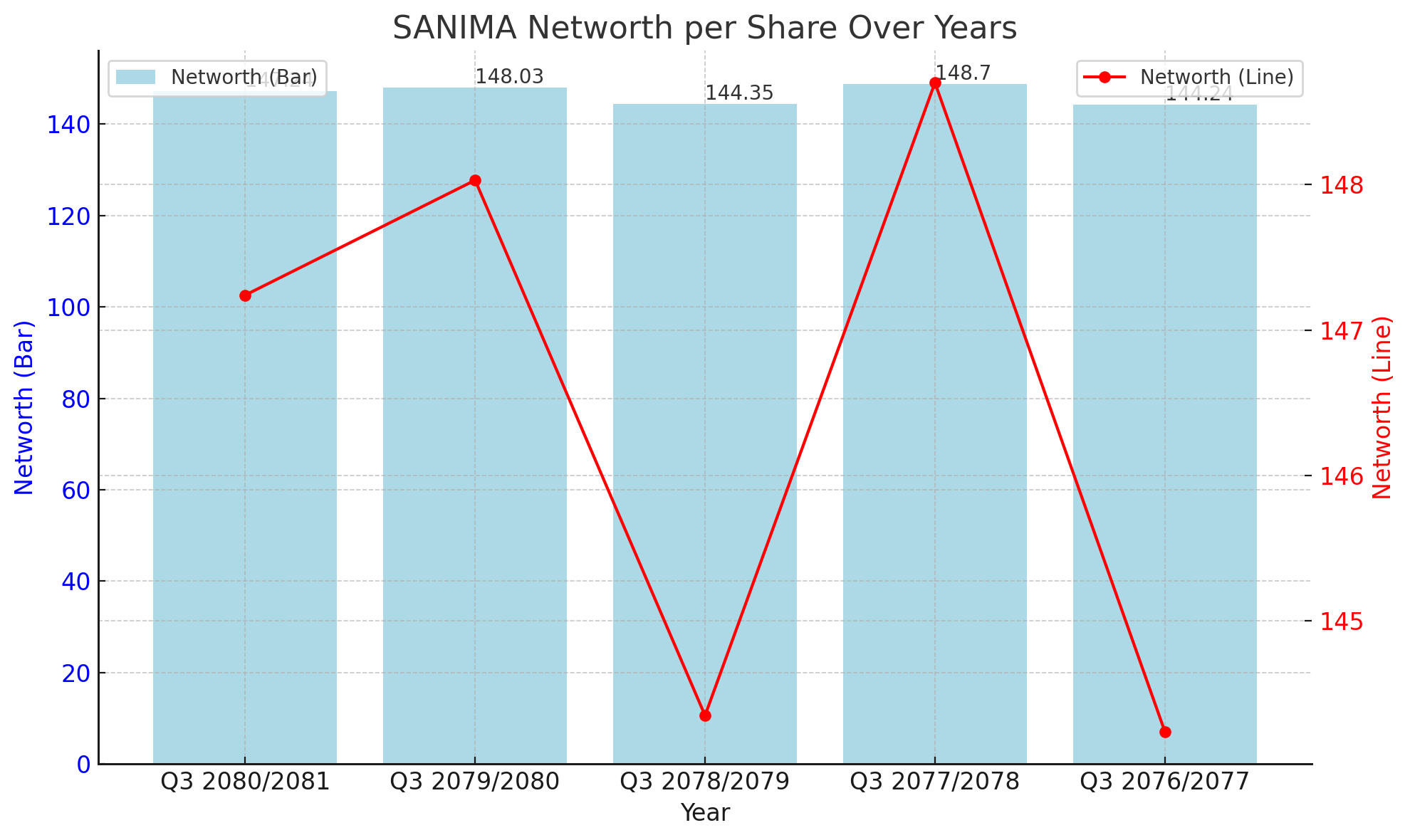

SANIMA Bank has maintained a relatively stable Networth per Share over the past five years, despite facing economic challenges that have impacted other financial metrics.

Q3 2076/2077: The Networth per Share was Rs. 144.24, reflecting a solid financial foundation and stable asset value.

Q3 2077/2078: The Networth per Share increased to Rs. 148.70, indicating growth in the bank's equity and asset value.

Q3 2078/2079: A slight decline to Rs. 144.35 was observed, possibly due to market adjustments or increased liabilities.

Q3 2079/2080: The Networth per Share saw a modest increase to Rs. 148.03, suggesting effective management of assets and liabilities despite external economic pressures.

Q3 2080/2081: The most recent data shows a slight decrease to Rs. 147.24, but the value remains close to the previous year's, indicating continued stability.

Overall, SANIMA Bank's Networth per Share has demonstrated resilience, with only minor fluctuations over the five-year period. This stability reflects the bank's strong asset management and ability to maintain its equity value despite facing economic challenges.

By maintaining a stable Networth per Share, SANIMA Bank continues to provide assurance to its investors and stakeholders about the bank's financial health and asset quality. As the bank navigates through various economic conditions, this stability will be crucial for its long-term growth and profitability.

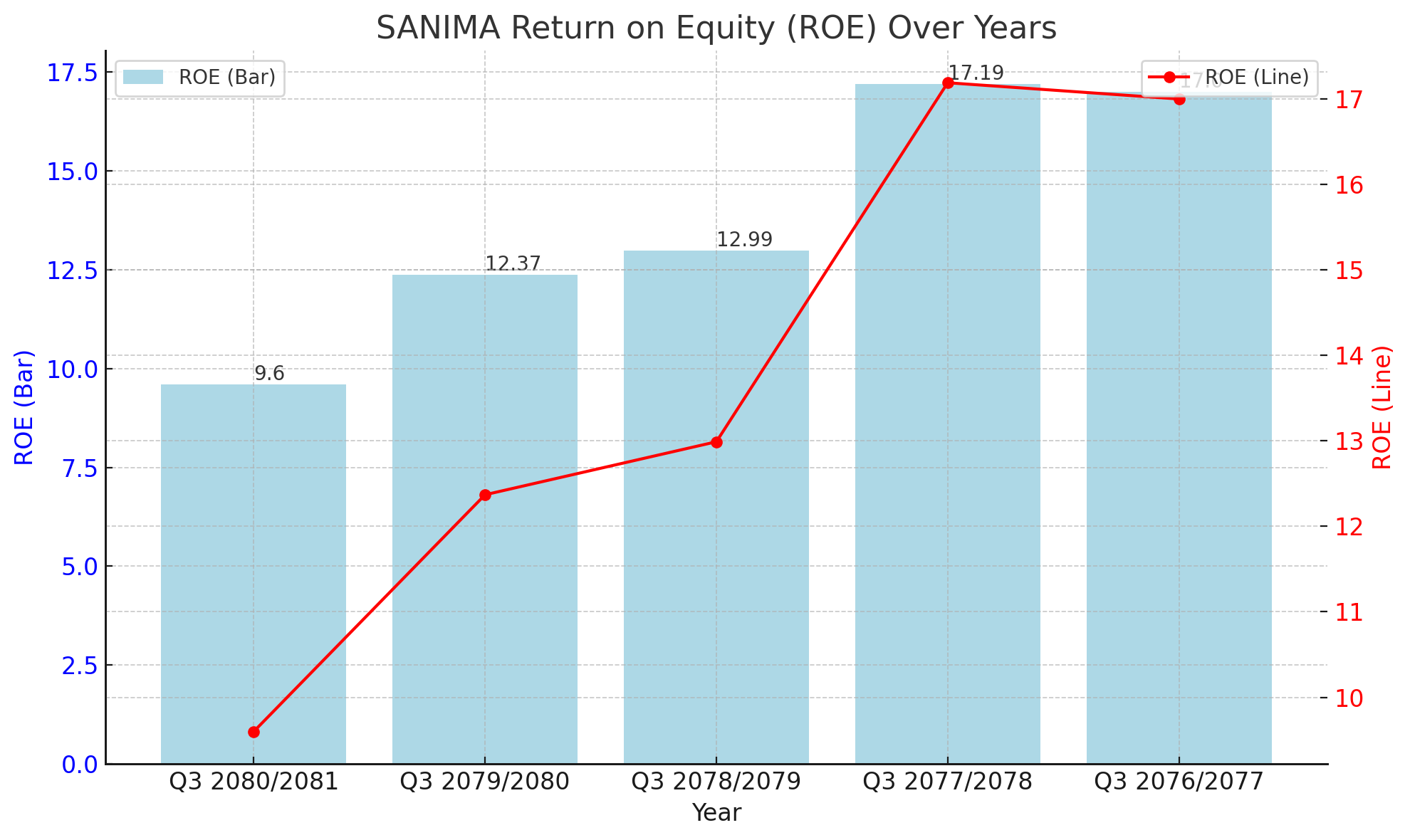

SANIMA Bank's Return on Equity Shows Declining Trend

SANIMA Bank's financial performance, as measured by its Return on Equity (ROE), has exhibited a noticeable decline over the past five years. This metric, which indicates how effectively the bank is generating profit from its shareholders' equity, provides insight into the bank's profitability and operational efficiency.

Q3 2076/2077: SANIMA Bank's ROE was 17%, indicating strong profitability and efficient use of equity.

Q3 2077/2078: The ROE increased slightly to 17.19%, suggesting continued strong performance and effective management of resources.

Q3 2078/2079: The ROE declined to 12.99%, marking the beginning of a downward trend. This decrease could be attributed to various factors, including increased competition, regulatory changes, or economic challenges.

Q3 2079/2080: The ROE further decreased to 12.37%, indicating continued challenges in maintaining profitability and efficient use of equity.

Q3 2080/2081: The most recent data shows a significant drop to 9.6%, highlighting substantial difficulties in generating profit from equity. This decline suggests the need for strategic adjustments to improve profitability and operational efficiency.

The consistent decline in SANIMA Bank's ROE over the last few years raises concerns about its ability to sustain profitability and effectively manage its resources. To address these challenges, SANIMA Bank may need to implement strategic initiatives focused on improving efficiency, exploring new revenue streams, and adapting to market changes.

Investors and stakeholders will be keenly observing SANIMA Bank's efforts to reverse this declining trend and restore its profitability and operational efficiency. The bank's ability to navigate these challenges will be crucial for its long-term growth and success.

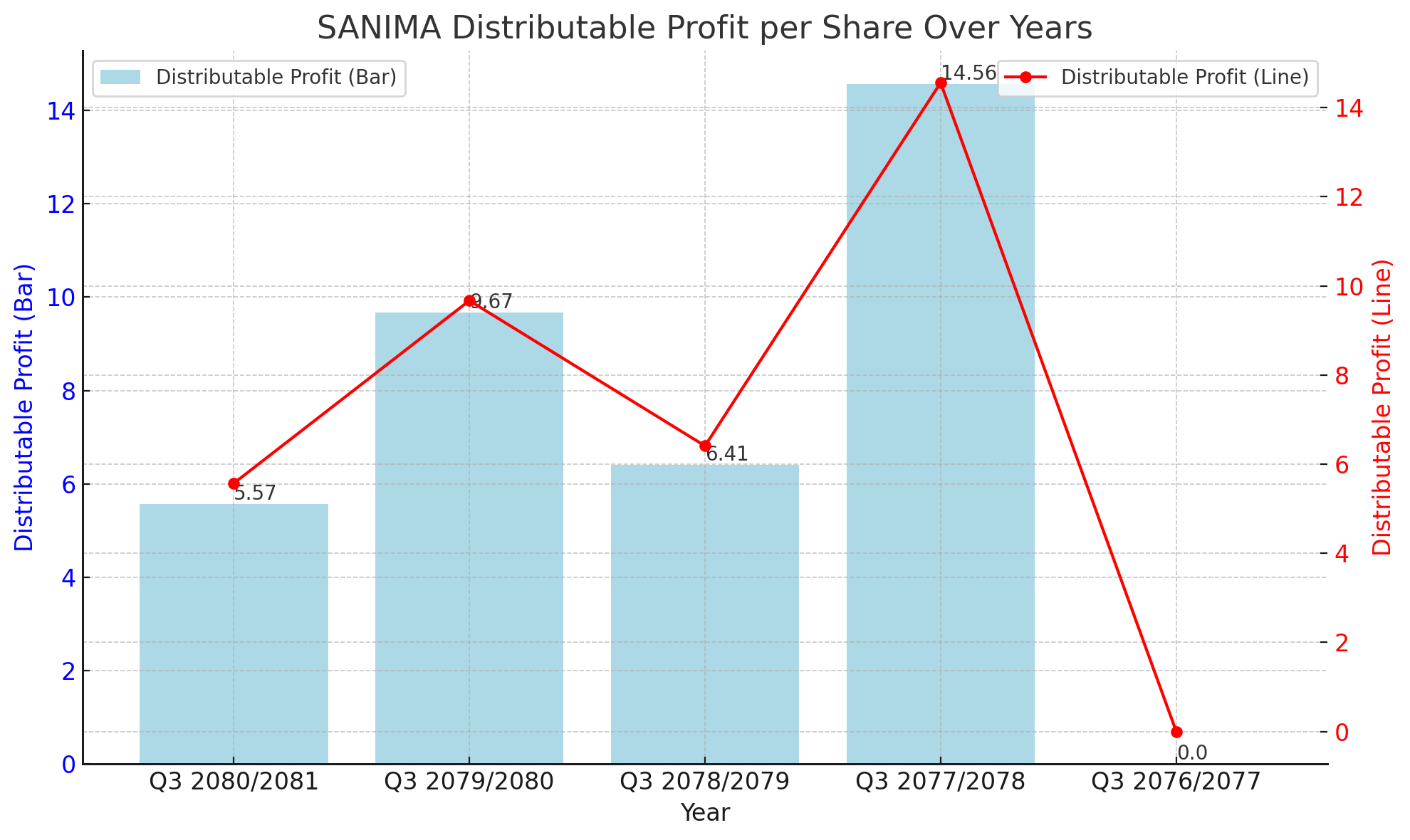

SANIMA Bank's financial performance, as measured by its Distributable Profit per Share, has shown considerable fluctuations over the past five years. This metric, which indicates the profit available for distribution to shareholders, provides insight into the bank's profitability and ability to reward its investors.

Q3 2076/2077: The bank reported a Distributable Profit per Share of Rs. 0, indicating no profit available for distribution to shareholders.

Q3 2077/2078: The Distributable Profit per Share increased significantly to Rs. 14.56, reflecting strong profitability and a substantial amount available for distribution.

Q3 2078/2079: The profit decreased to Rs. 6.41, marking a sharp decline from the previous year. This decrease could be attributed to various factors, including increased expenses, lower revenues, or changes in profit allocation policies.

Q3 2079/2080: The Distributable Profit per Share saw an increase to Rs. 9.67, indicating some recovery and improvement in profitability.

Q3 2080/2081: The most recent data shows a decline to Rs. 5.57, highlighting ongoing challenges in maintaining profitability and distributing profit to shareholders.

The fluctuations in SANIMA Bank's Distributable Profit per Share over the last five years suggest a need for strategic adjustments to stabilize and improve profitability. Investors and stakeholders will be closely monitoring the bank's efforts to enhance its financial performance and provide consistent returns.

Dipesh Ghimire

·8 Apr, 2026