By Writer Content

SBI Financial Analysis: Navigating EPS, NPL, Networth, ROE, and Distributable Profit Trends

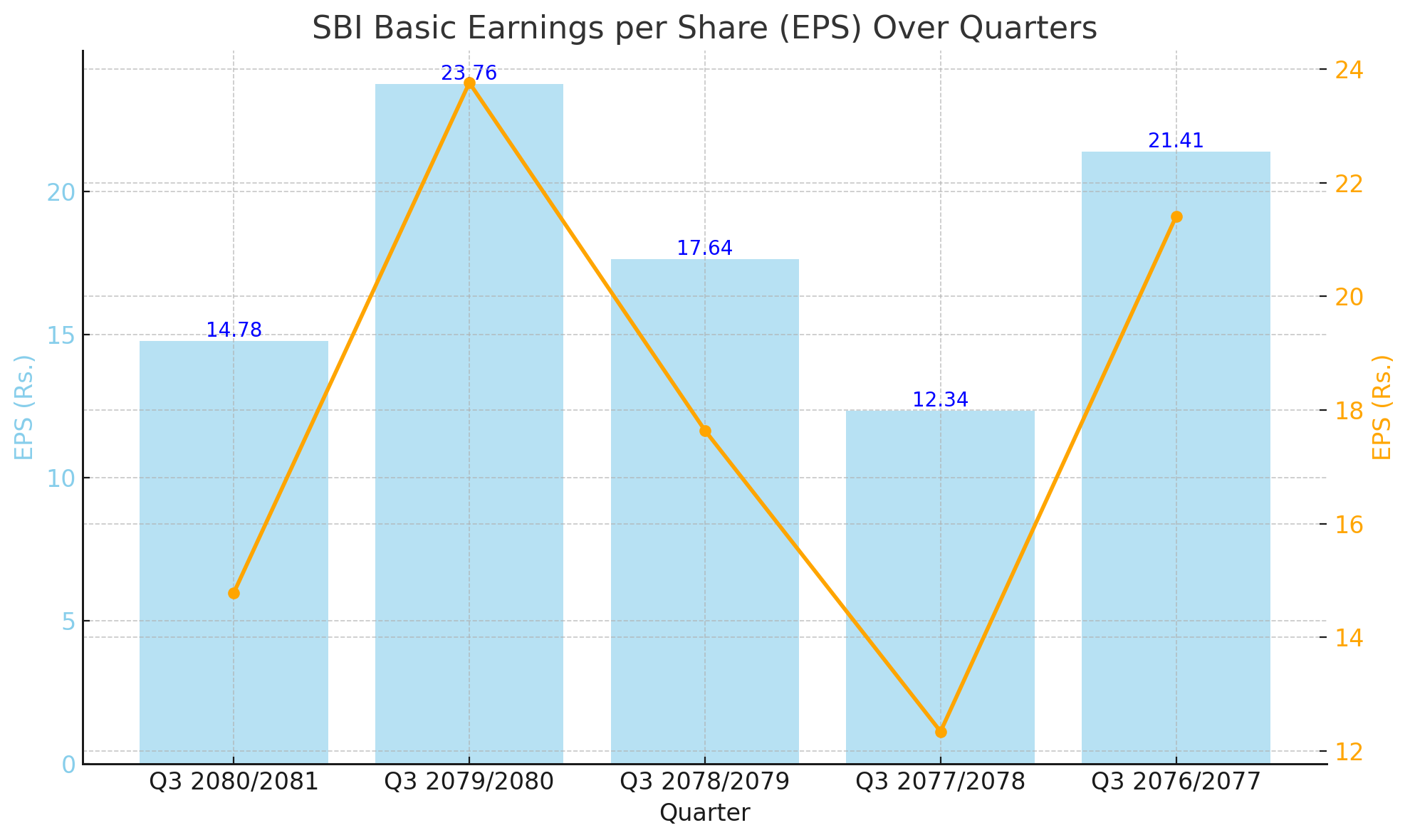

EPS Trends and Interpretation

The EPS for Q3 2080/2081 stood at Rs. 14.78, a significant decline from Rs. 23.76 reported in Q3 2079/2080. This drop indicates potential challenges faced by the bank, possibly due to increased operational costs, economic slowdown, or competitive pressures impacting profitability. Despite this decrease, the bank’s EPS remained above the figures from Q3 2077/2078, which recorded an EPS of Rs. 12.34, suggesting that while the recent performance has been less than ideal, it still surpasses some of the previous years' lows.

In Q3 2079/2080, the EPS peaked at Rs. 23.76, marking the highest performance in the observed period. This surge could be attributed to strategic initiatives, improved market conditions, or successful cost management during that fiscal year. However, the following year’s EPS dropped to Rs. 17.64 in Q3 2078/2079, and further to Rs. 12.34 in Q3 2077/2078, reflecting a period of instability and potential operational inefficiencies or market disruptions that affected the bank’s earnings.

Interestingly, the EPS rebounded to Rs. 21.41 in Q3 2076/2077, showing a recovery phase where the bank might have implemented effective measures to boost profitability. This rebound demonstrates SBI's resilience and capability to recover from financial setbacks, likely through enhanced revenue streams, cost-cutting measures, or successful market strategies.

Economic Implications

The fluctuating EPS figures underscore the challenges and opportunities within the banking sector, particularly in a dynamically changing economic environment. The high EPS of Rs. 23.76 in Q3 2079/2080 reflects a period of strong financial health and market confidence in SBI’s strategies. In contrast, the decline to Rs. 14.78 in the most recent quarter highlights the need for continuous adaptation and strategic foresight to navigate economic uncertainties and maintain shareholder value.

Strategic Outlook

For investors and stakeholders, understanding these EPS trends is crucial for making informed decisions. The bank’s ability to rebound and show resilience after periods of decline suggests a robust underlying business model capable of withstanding economic pressures. Moving forward, SBI may need to focus on stabilizing its earnings through diversified revenue channels, technological advancements, and maintaining a strong competitive edge in the banking sector.

Conclusion

SBI’s EPS performance over the last five quarters presents a mixed picture of highs and lows, reflecting both the challenges and resilience of the bank. The latest figures call for strategic measures to ensure sustainable growth and profitability, reinforcing the importance of adaptability in a volatile economic landscape. Investors will keenly observe SBI's upcoming fiscal reports for indications of stability and growth potential.

NPL Trends and Interpretation

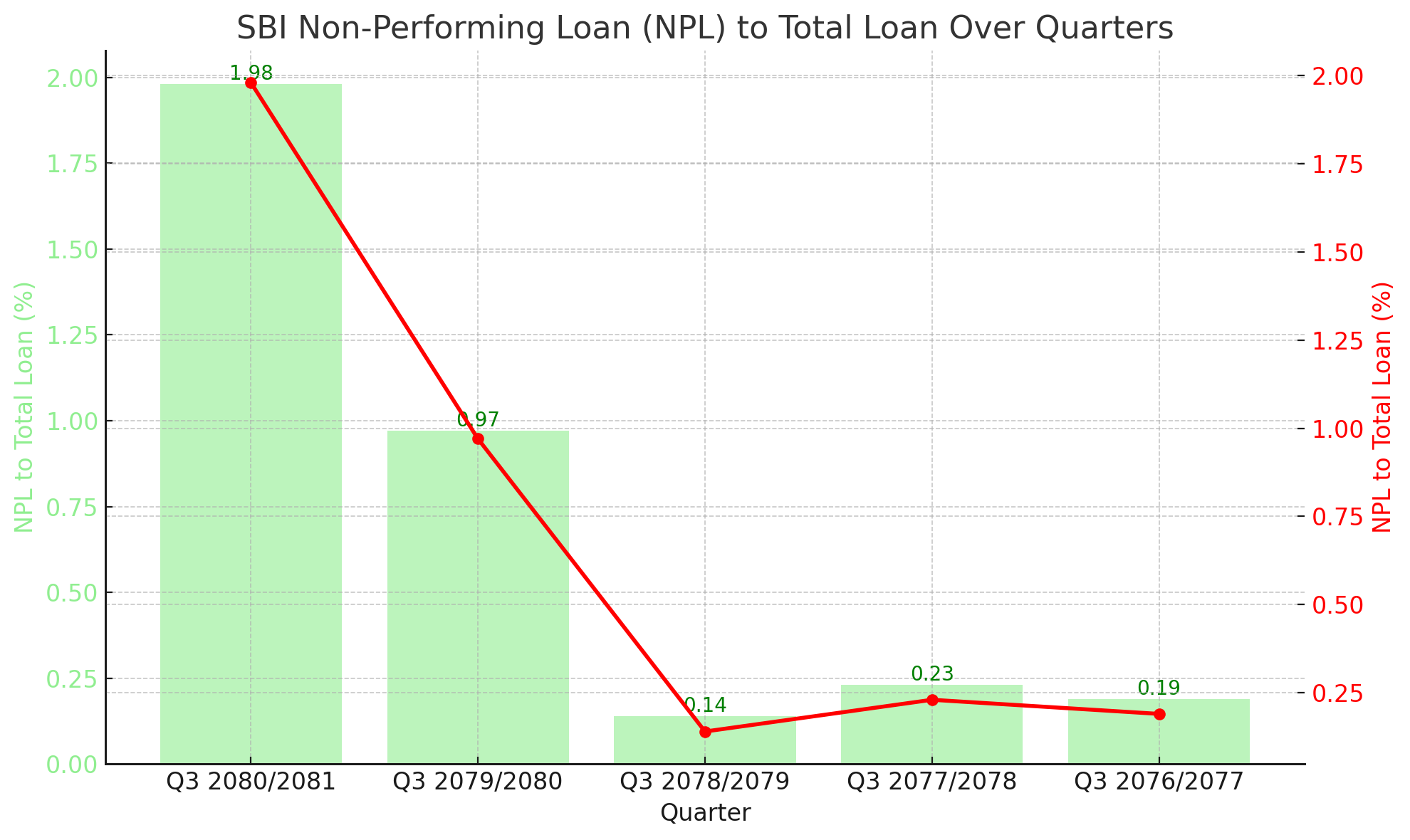

The NPL to total loan ratio for Q3 2080/2081 stands at 1.98%, marking a sharp increase from the 0.97% reported in Q3 2079/2080. This uptick suggests that SBI is facing growing challenges in maintaining the quality of its loan portfolio. Higher NPL ratios typically indicate increased defaults on loans, which can impact the bank's profitability and financial stability.

In Q3 2079/2080, the NPL ratio was relatively low at 0.97%, reflecting better loan performance and effective risk management practices during that period. However, the subsequent quarters show a worrying trend, with the NPL ratio spiking dramatically. The lowest NPL ratio was recorded in Q3 2078/2079 at just 0.14%, suggesting a period of robust loan performance and minimal defaults.

Interestingly, prior to the recent surge, the NPL ratios in Q3 2077/2078 and Q3 2076/2077 were relatively stable at 0.23% and 0.19%, respectively. This indicates that SBI had been maintaining a consistent loan quality before the recent deterioration.

Economic Implications

The rising NPL ratio poses several economic implications for SBI and its stakeholders. An increasing NPL ratio can lead to higher provisioning costs for bad loans, eroding the bank's profitability. It also reflects underlying economic stress, potentially hinting at broader issues such as economic slowdown, poor borrower performance, or ineffective credit risk management.

The significant jump in the NPL ratio for the latest quarter highlights the need for SBI to strengthen its loan recovery mechanisms and enhance credit risk assessment processes. Failure to address the rising NPL levels could result in diminished investor confidence and potential regulatory scrutiny.

Strategic Outlook

For investors and analysts, monitoring the NPL trends is crucial for assessing the bank's financial health and risk exposure. The sharp increase in NPL ratio warrants a closer examination of SBI's loan portfolio and credit practices. The bank may need to implement stringent measures to curb the rise in bad loans, such as improved borrower vetting, enhanced recovery processes, and robust credit monitoring systems.

SBI's management will need to reassure investors by outlining a clear strategy to address the rising NPLs and restore loan quality. This could involve targeted recovery efforts, restructuring of troubled loans, and diversifying the loan portfolio to mitigate risk.

Conclusion

SBI's latest financial data reveals a concerning rise in Non-Performing Loan ratio, indicating increased challenges in loan performance and potential financial stress. The bank's ability to manage and mitigate these risks will be critical in maintaining financial stability and investor confidence. As SBI navigates these challenges, stakeholders will be keenly observing the bank's strategic response and its impact on future financial performance.

Networth per Share Trends and Interpretation

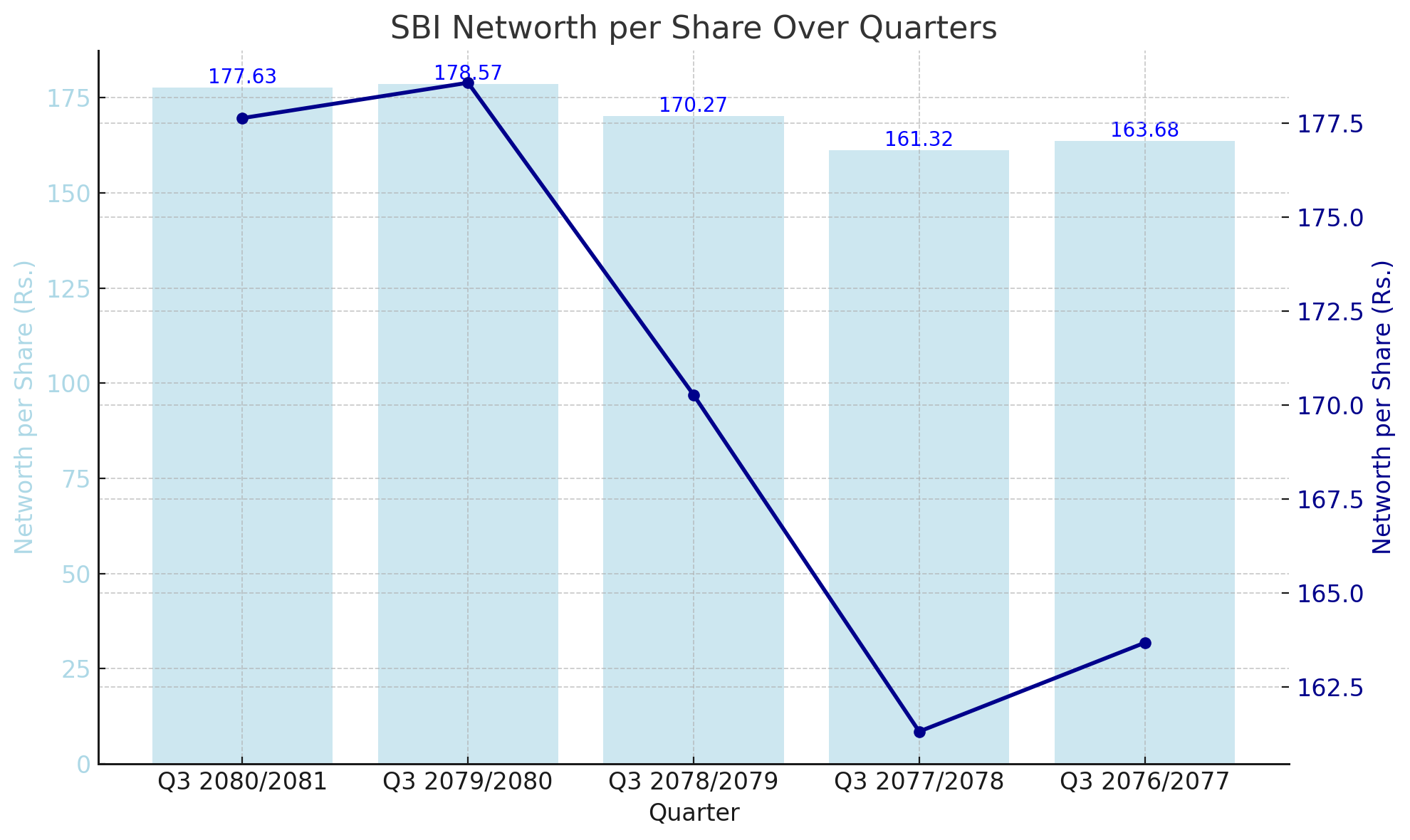

For the quarter ending Q3 2080/2081, SBI reported a Networth per Share of Rs. 177.63, slightly down from Rs. 178.57 in Q3 2079/2080. This minor decrease suggests that while there have been slight variances, SBI has managed to maintain its net worth at a robust level, indicating solid asset management and equity retention practices.

In Q3 2079/2080, the Networth per Share peaked at Rs. 178.57, marking the highest value in the observed period. This peak indicates a period of strong financial health and effective capital management. The subsequent quarter, Q3 2078/2079, saw a slight dip to Rs. 170.27, reflecting minor changes in the bank's financial structure or asset valuation.

Earlier quarters, Q3 2077/2078 and Q3 2076/2077, recorded Networth per Share values of Rs. 161.32 and Rs. 163.68, respectively. These figures highlight a period of gradual improvement, showcasing SBI's steady growth and strengthening financial position over time.

Economic Implications

The stable Networth per Share over the recent quarters underscores SBI’s resilience and effective financial strategies. A consistent net worth reflects the bank's ability to retain earnings, manage assets efficiently, and maintain shareholder equity. This stability is particularly significant in the banking sector, where fluctuations in financial metrics can impact investor confidence and market perceptions.

The slight dip in the latest quarter compared to the peak in Q3 2079/2080 suggests that while the bank is performing well, there may be external factors or internal adjustments affecting its net worth. These could include changes in market conditions, strategic investments, or shifts in asset valuations.

Strategic Outlook

For investors and stakeholders, the steady Networth per Share is a positive indicator of SBI’s financial health and stability. It suggests that the bank has been successful in navigating economic challenges and maintaining a strong financial foundation. Moving forward, SBI may focus on further enhancing its asset management practices and exploring opportunities for growth to continue improving its net worth.

SBI's management should continue to monitor and adapt to market conditions, ensuring that strategic decisions align with long-term financial goals. Maintaining transparency and effective communication with shareholders will be crucial in sustaining investor confidence.

Conclusion

SBI’s performance in terms of Networth per Share reflects a stable and resilient financial position. Despite minor fluctuations, the bank has demonstrated effective asset management and capital retention. As SBI moves forward, its strategic focus on maintaining financial health and exploring growth opportunities will be key to sustaining and enhancing its net worth.

ROE Trends and Interpretation

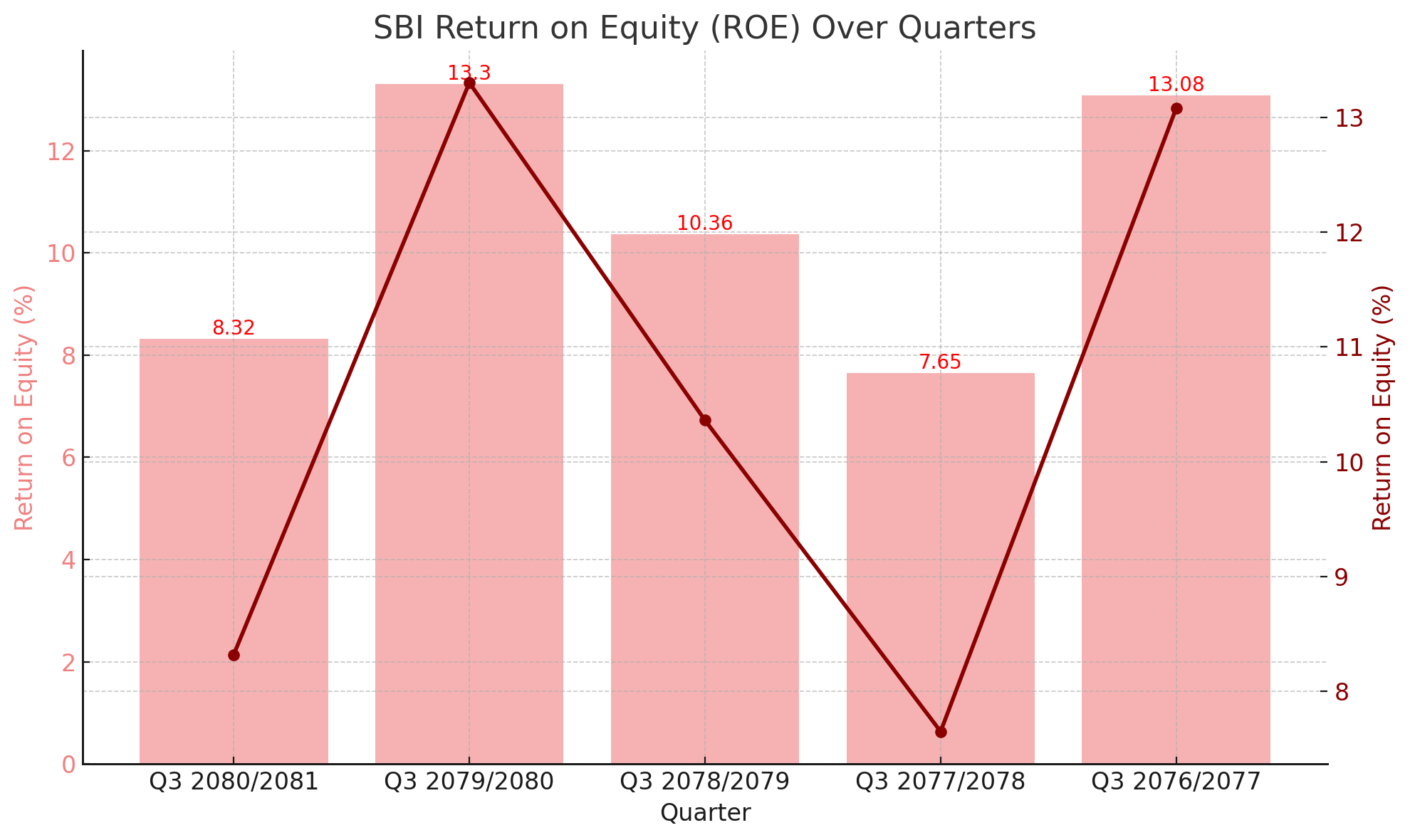

For the quarter ending Q3 2080/2081, SBI reported an ROE of 8.32%, a noticeable decline from 13.3% in Q3 2079/2080. This decrease indicates reduced profitability and potential challenges in generating returns on shareholders' investments during this period.

In Q3 2079/2080, the ROE peaked at 13.3%, marking the highest return in the observed period. This peak suggests a period of robust financial performance and effective utilization of equity to generate profits. However, the subsequent quarters show a downward trend, with the ROE dropping to 10.36% in Q3 2078/2079 and further to 7.65% in Q3 2077/2078, indicating challenges in maintaining high profitability levels.

Interestingly, Q3 2076/2077 recorded an ROE of 13.08%, which is comparable to the peak in Q3 2079/2080. This reflects a previous period of strong financial performance, showcasing the bank's capability to achieve high returns on equity under favorable conditions.

Economic Implications

The fluctuating ROE values underscore the challenges faced by SBI in maintaining consistent profitability. A declining ROE can impact investor confidence and signal potential inefficiencies in utilizing equity to generate returns. The sharp drop in ROE for the most recent quarter suggests that SBI may need to revisit its strategies and focus on improving operational efficiency and profitability.

The high ROE in Q3 2079/2080 and Q3 2076/2077 highlights SBI’s ability to achieve substantial returns under favorable conditions. These peaks reflect periods of strong financial health and effective management practices. However, the volatility in ROE indicates that maintaining such performance consistently is challenging, necessitating continuous strategic adjustments.

Strategic Outlook

For investors and stakeholders, the fluctuating ROE is a crucial indicator of SBI's financial health and operational efficiency. The recent decline calls for strategic measures to enhance profitability and ensure effective utilization of equity. SBI may need to focus on optimizing its cost structure, improving revenue streams, and enhancing risk management practices to stabilize and improve ROE.

SBI's management should communicate its strategic plans to address the declining ROE and restore investor confidence. Transparent and effective communication about the steps being taken to enhance profitability and efficiency will be critical in maintaining shareholder trust and market confidence.

Conclusion

SBI’s fluctuating ROE over the recent quarters reflects the challenges and opportunities faced by the bank in maintaining profitability. The recent decline highlights the need for strategic measures to enhance financial performance and ensure effective utilization of equity. As SBI navigates these challenges, its ability to implement and communicate effective strategies will be key to sustaining and improving its ROE.

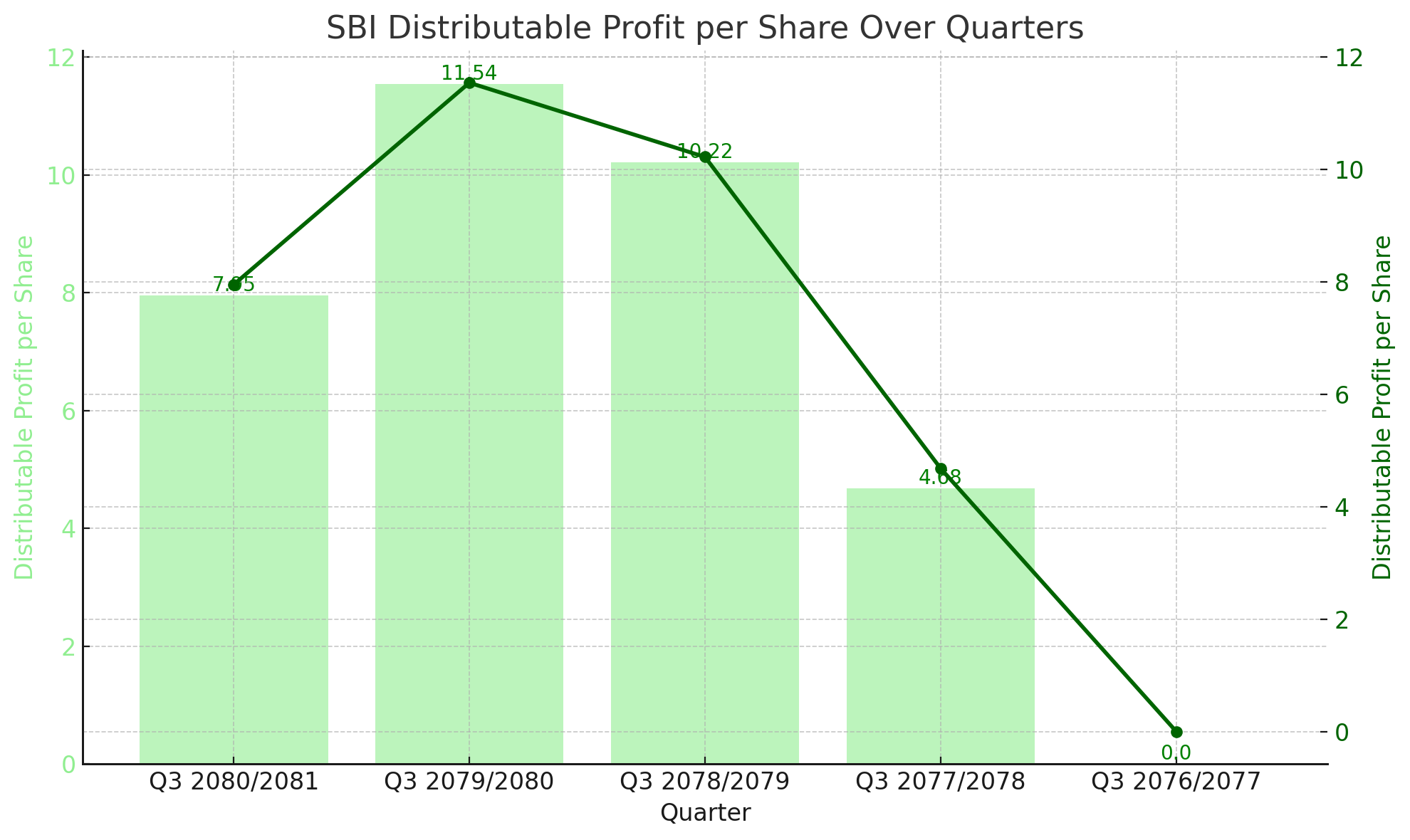

SBI Reports Decrease in Distributable Profit per Share Over Recent Quarters

For the quarter ending Q3 2080/2081, SBI reported a Distributable Profit per Share of Rs. 7.95, a decrease from Rs. 11.54 in Q3 2079/2080. This decline indicates reduced distributable earnings, possibly due to lower overall profits or increased allocations to reserves and provisions.

In Q3 2079/2080, the Distributable Profit per Share peaked at Rs. 11.54, marking the highest value in the observed period. This peak suggests a period of strong profitability and efficient financial management, allowing for a higher portion of profits to be allocated for distribution to shareholders. However, the subsequent quarter, Q3 2078/2079, saw a decline to Rs. 10.22, reflecting a drop in distributable earnings.

The previous quarters, Q3 2077/2078 and Q3 2076/2077, recorded Distributable Profit per Share values of Rs. 4.68 and Rs. 0, respectively. The zero value in Q3 2076/2077 indicates that no profits were available for distribution, possibly due to operational losses or complete reinvestment of earnings.

Economic Implications

The fluctuating Distributable Profit per Share values highlight the challenges faced by SBI in maintaining consistent profitability and the ability to allocate profits for distribution. The decrease in recent quarters suggests potential pressures on the bank’s earnings, which could impact investor confidence and shareholder returns.

The high distributable profit in Q3 2079/2080 reflects a period of robust financial health and effective earnings management. Conversely, the decline in subsequent quarters underscores the need for SBI to enhance its profitability and optimize its financial strategies to ensure stable and growing returns for shareholders.

Strategic Outlook

For investors and stakeholders, the trends in Distributable Profit per Share are critical indicators of SBI’s financial health and its ability to generate and distribute earnings. The recent decline calls for strategic measures to boost profitability and ensure a steady flow of distributable earnings. SBI may need to focus on revenue growth, cost optimization, and efficient capital allocation to improve its financial performance.

SBI's management should communicate its plans to address the declining distributable profits and reassure investors of its commitment to enhancing shareholder value. Transparent and proactive communication about strategic initiatives and expected financial outcomes will be crucial in maintaining investor trust and confidence.

Conclusion

SBI’s declining Distributable Profit per Share over the recent quarters reflects the bank’s challenges in maintaining consistent profitability and distributable earnings. The recent decline highlights the need for strategic measures to enhance financial performance and ensure stable returns for shareholders. As SBI navigates these challenges, its ability to implement and communicate effective strategies will be key to sustaining and improving distributable profits.