Top

Hot

Popular

NEPSE Trading

Stock

Trading

Dipesh Ghimire

Peer-to-Peer (P2P) Lending: A Revolution in Alternative Finance

Peer-to-Peer (P2P) Lending: A Revolution in Alternative Finance In today’s digital economy, Peer-to-Peer (P2P) lending has emerged as a significant alternative to traditional banking. It enables individuals to lend and borrow money directly through online platforms without the involvement of conventional financial institutions. This model is transforming the financial landscape by increasing access to credit while offering lenders attractive returns. However, P2P lending also comes with risks that must be carefully managed through regulatory oversight and responsible investing.

Dipesh Ghimire

3 min read

In today’s digital economy, Peer-to-Peer (P2P) lending has emerged as a significant alternative to traditional banking. It enables individuals to lend and borrow money directly through online platforms without the involvement of conventional financial institutions. This model is transforming the financial landscape by increasing access to credit while offering lenders attractive returns. However, P2P lending also comes with risks that must be carefully managed through regulatory oversight and responsible investing.

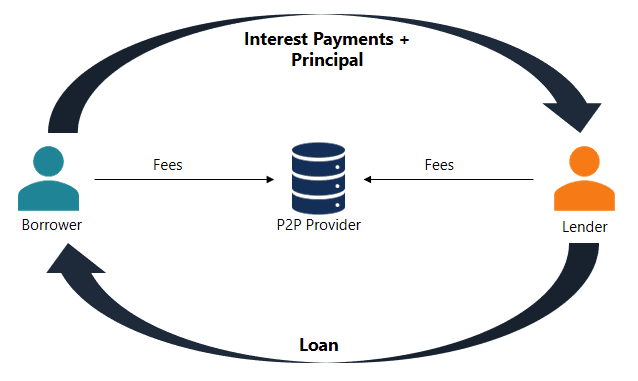

How P2P Lending Works

P2P lending connects lenders and borrowers through a digital platform. The lender provides funds expecting interest-based returns, while the borrower accesses credit without the stringent requirements of traditional banks. A P2P lending platform acts as an intermediary, conducting credit assessments, setting interest rates, and handling transactions. However, unlike banks, these platforms do not take on the risk themselves; instead, individual lenders assume the risk.

This form of lending benefits both parties:

For lenders, it provides an opportunity to earn higher interest rates than conventional savings accounts or fixed deposits.

For borrowers, especially small businesses and individuals with limited credit history, P2P lending offers a viable alternative to bank loans.

Regulation and Risks in P2P Lending

Despite its advantages, P2P lending carries risks. Since these loans do not have traditional banking protections, lenders face a higher risk of default. The platform mitigates this by assessing borrower creditworthiness, but there are no guarantees on loan recovery if the borrower defaults.

Regulatory authorities worldwide are introducing measures to ensure that P2P lending operates within a safe financial environment. Countries like the United Kingdom, United States, and India have established specific guidelines for P2P lending platforms, mandating risk disclosures and capital adequacy requirements. In Nepal, regulatory discussions are still in progress, as the country assesses how to integrate P2P lending within its financial system without jeopardizing stability.

Crowdfunding vs. P2P Lending

P2P lending is often confused with crowdfunding, but they differ fundamentally. While P2P lending involves debt financing, crowdfunding allows multiple individuals to contribute funds for a project, business, or social cause without expecting repayment. Crowdfunding can be:

Donation-based – Supporting social causes without financial returns.

Equity-based – Investors receive a stake in the company.

Reward-based – Funders get early access to products or services.

In contrast, P2P lending follows a structured loan-repayment model, making it a viable alternative to traditional loans.

Future of P2P Lending in Nepal

Nepal’s financial sector is still largely reliant on traditional banking, but alternative financing models like P2P lending could play a crucial role in expanding credit access. Given Nepal’s growing digital economy and increasing demand for financial inclusion, P2P lending could support startups, small businesses, and underserved communities.

However, proper regulatory frameworks must be in place to manage risks such as fraud, defaults, and unfair lending practices. The Nepal Rastra Bank (NRB), the country’s central bank, is closely monitoring global trends before introducing formal regulations.

Interpretation: Will P2P Lending Disrupt Traditional Banking?

P2P lending represents a shift in the financial ecosystem, challenging the dominance of banks in credit distribution. It offers an agile, tech-driven alternative that could democratize finance, particularly in developing economies like Nepal. However, for this model to succeed, investor education, regulatory clarity, and strong risk assessment mechanisms must be established.

The question remains: Will P2P lending replace traditional banks? Not entirely. Instead, it is likely to complement the existing financial system, providing alternative funding sources while encouraging banks to innovate and adopt digital lending models. If properly managed, P2P lending could unlock new economic opportunities and transform Nepal’s financial landscape.

Written by

Dipesh Ghimire

Related News