Banking Industry

History of Banking Industry in Nepal

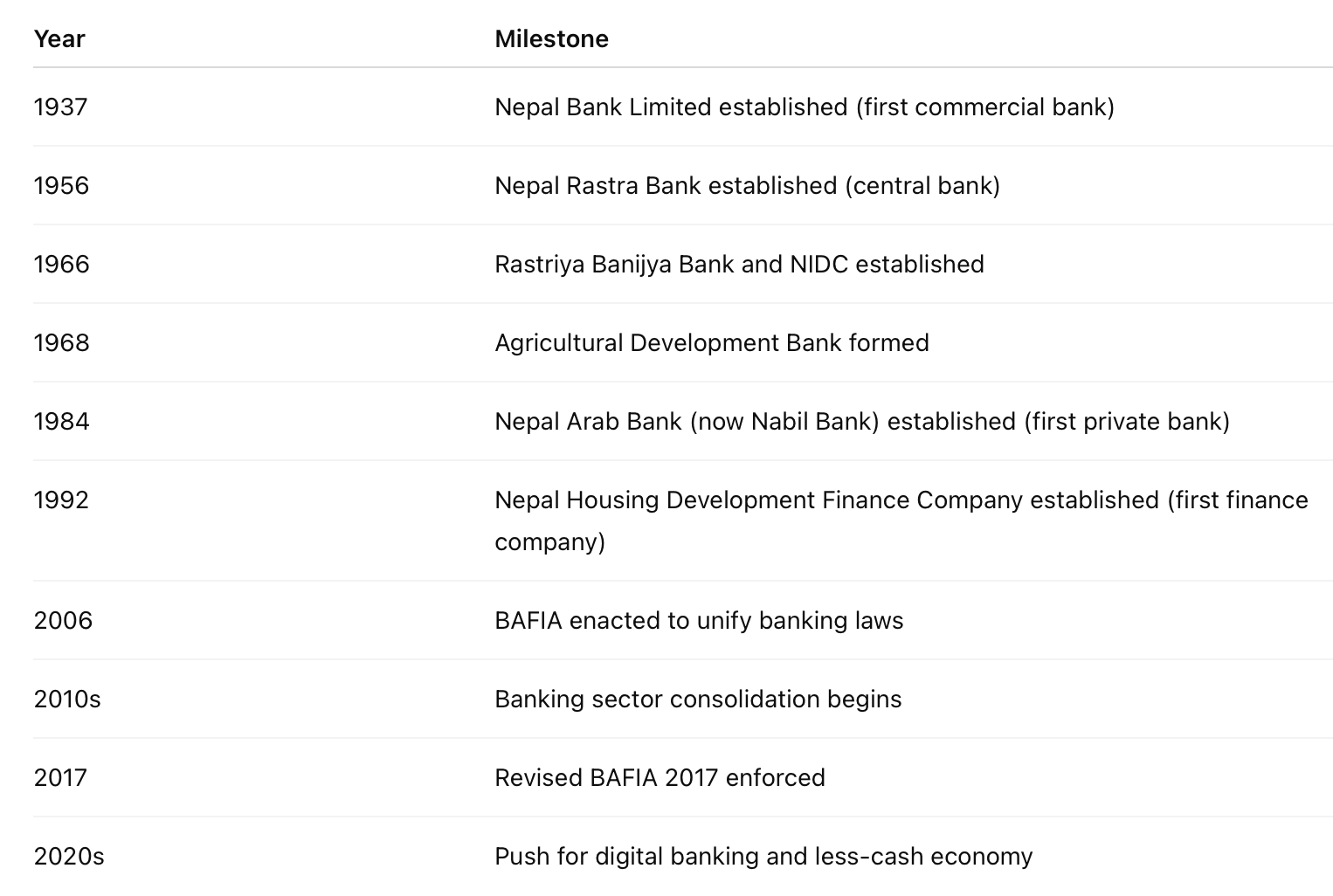

Nepal’s banking industry began in 1937 with the establishment of Nepal Bank Limited, the first commercial bank. The Nepal Rastra Bank, the country's central bank, was founded in 1956 to regulate monetary policy and issue currency. Over the decades, Nepal saw the creation of key institutions like Rastriya Banijya Bank (1966), Agricultural Development Bank (1968), and Nepal Industrial Development Corporation (1959). Financial liberalization in the 1980s and 1990s led to the rise of private banks, including Nepal Arab Bank (now Nabil Bank), and the introduction of finance companies. The Bank and Financial Institutions Act (BAFIA) of 2006 and its 2017 revision unified Nepal’s banking regulations. In recent years, the focus has shifted to digital banking, promoting QR and card-based payments, and reducing the number of banks through consolidation to strengthen the financial system.

Sandeep Chaudhary

3 min read

The history of Nepal’s banking industry traces back to 1937, with the establishment of Nepal Bank Limited (NBL)—the first commercial bank in the country. Formed under the then Nepal Bank Act (1937) as a public-private partnership, NBL marked the beginning of formal banking in Nepal. Notably, this was nearly two decades before the establishment of Nepal’s central bank.

In 1956, the Nepal Rastra Bank (NRB) was established under the Nepal Rastra Bank Act (1955) as the central bankof the country. NRB’s primary mandate was to issue banknotes, stabilize the exchange rate, and guide the country’s monetary and financial policy. In 2002, a revised NRB Act was introduced, which expanded the bank’s responsibilities to include ensuring price stability, maintaining external sector stability, and promoting public confidence in the financial system.

Recognizing the need for industrial development, the government established the Industrial Development Centre in 1959, which later evolved into the Nepal Industrial Development Corporation (NIDC) in 1966 under a dedicated act. NIDC served as Nepal’s first development bank, until it was eventually merged with Rastriya Banijya Bank (RBB) in 2018.

The momentum of institutional banking growth continued with the establishment of Rastriya Banijya Bank (RBB) in 1966, under the RBB Act (1965). Later, both NBL and RBB were brought under a common regulatory framework through the Commercial Bank Act (1974).

In 1968, the government launched the Agricultural Development Bank Nepal (ADB/N) through the Agricultural Development Bank Act (1967). This involved the merger of the Cooperative Development Bank (1963) and later, the Land Reform and Savings Institution (1973), to create a comprehensive rural and agricultural financing institution.

Financial Liberalization and Private Sector Entry

The 1980s marked a pivotal period as Nepal began liberalizing its financial sector. This included interest rate deregulation, allowing private sector bank licenses, and the restructuring of state-owned banks. A landmark in this reform was the establishment of Nepal Arab Bank Limited (now Nabil Bank) in 1984, the first private and foreign joint-venture commercial bank in Nepal.

To meet growing demands for consumer and housing finance, the Finance Company Act was passed in 1985. This led to the formation of Nepal Housing Development Finance Company in 1992, the first finance company in Nepal. Its establishment triggered a wave of new finance companies across the country.

Consolidation and Modern Regulatory Framework

As the number of banks and financial institutions (BFIs) expanded rapidly through the 1990s and early 2000s, regulatory challenges emerged. To streamline and regulate the industry, the government introduced the Bank and Financial Institutions Act (BAFIA) in 2006, which acted as an umbrella law replacing all previous institution-specific acts. This was further revised and re-enacted as BAFIA 2017, reinforcing the central bank's oversight powers.

In the early 2010s, NRB adopted a banking sector consolidation policy, encouraging mergers and acquisitions among financial institutions to create stronger, more resilient banks. As a result, the number of BFIs significantly declined, but their capital base, outreach, and technology adoption improved.

Digitalization and Future Outlook

In recent years, the NRB and Nepal’s banking industry have been pushing towards a less-cash economy. The promotion of digital payment systems, such as QR-code and card-based retail transactions, is at the forefront of this transformation. The goal is not only to modernize banking services but also to expand financial inclusion and strengthen the overall economic infrastructure of the country.

Written by

Sandeep Chaudhary