By Writer Content

MBL Financial Challenges: Declining EPS, Rising NPLs, and ROE

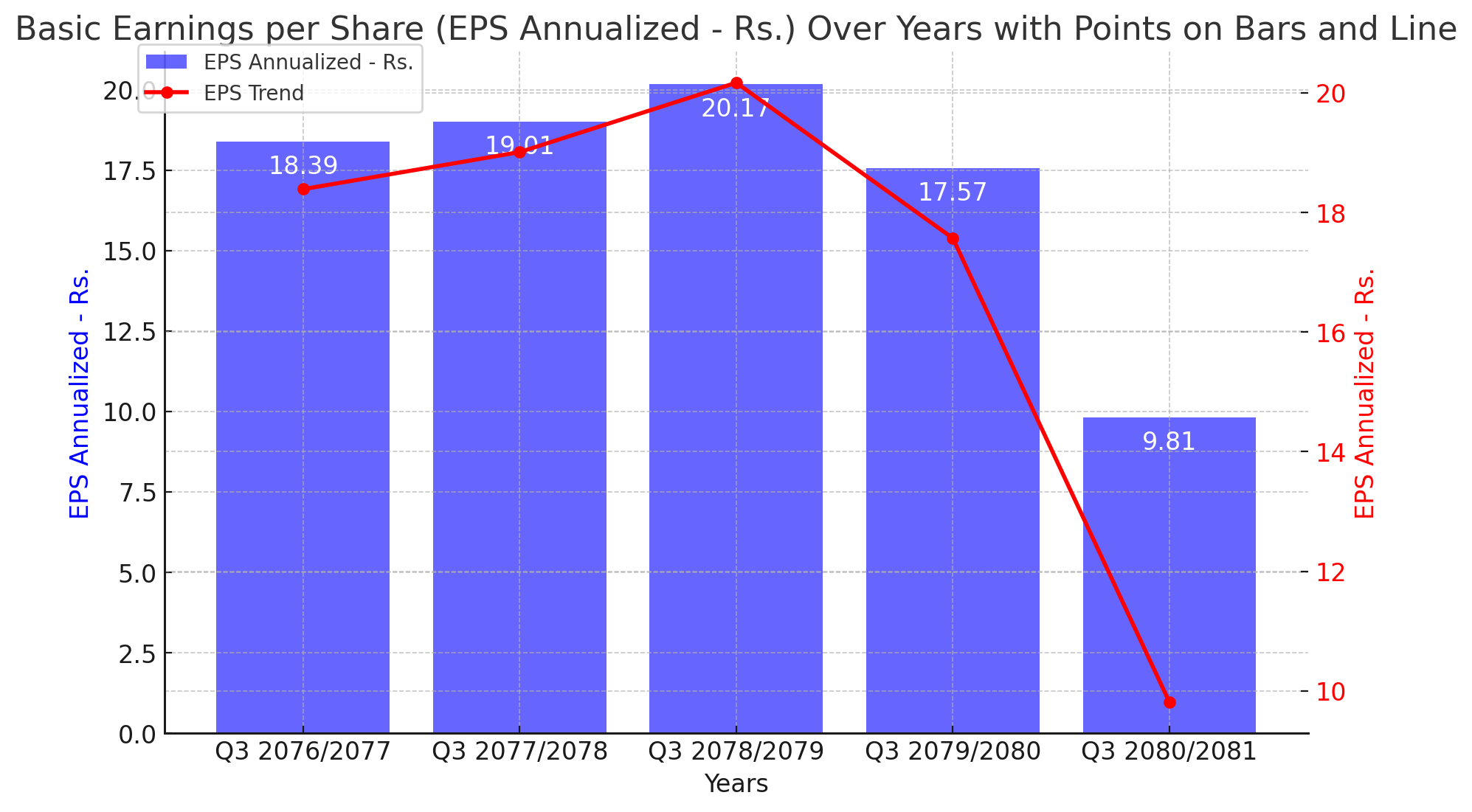

Article Title: MBL's Basic Earnings per Share Declines Significantly in Q3 2080/2081

In a notable shift, MBL's Basic Earnings per Share (EPS) has seen a substantial decline in the third quarter of the fiscal year 2080/2081. This marked decline is a departure from the generally steady performance observed over the past few years.

Analysis of EPS Over Five Years

The EPS for Q3 2080/2081 stands at 9.81, a sharp decrease from the previous year's 17.57. This downward trend is particularly concerning when contrasted with the peak EPS of 20.17 recorded in Q3 2078/2079. Over the past five years, MBL's EPS has demonstrated the following pattern:

- Q3 2076/2077: 18.39

- Q3 2077/2078: 19.01

- Q3 2078/2079: 20.17

- Q3 2079/2080: 17.57

- Q3 2080/2081: 9.81

Interpretation of the Data

The decline from 20.17 in Q3 2078/2079 to 9.81 in Q3 2080/2081 is significant. This drop could be attributed to a myriad of factors, including market conditions, operational challenges, and broader economic impacts. The EPS serves as an indicator of a company's profitability, and a declining EPS suggests that MBL has faced difficulties in maintaining its earnings.

Possible Factors Contributing to the Decline

1. Market Conditions: The overall economic environment and market conditions can greatly influence a company's earnings. If the financial market has experienced volatility or a downturn, this could impact MBL's profitability.

2. Operational Challenges: Internal factors such as increased operational costs, inefficiencies, or disruptions could also lead to reduced earnings. MBL may need to assess its operational strategies to identify areas for improvement.

3. Competition: Increased competition in the banking sector might have exerted pressure on MBL's margins, leading to lower profitability.

4. Regulatory Changes: Any recent changes in banking regulations could have impacted MBL's earnings, either through increased compliance costs or through constraints on its operations.

Moving Forward

For MBL, the focus should be on identifying the core reasons behind this decline and addressing them proactively. Enhancing operational efficiency, exploring new revenue streams, and adapting to market conditions will be crucial. Furthermore, maintaining transparent communication with shareholders and stakeholders about the challenges and strategies being implemented to overcome them will be important for maintaining confidence.

Conclusion

The significant decline in MBL's Basic Earnings per Share in Q3 2080/2081 is a critical issue that warrants thorough analysis and strategic action. While the past performance has shown resilience, the recent downturn highlights the need for adaptive measures to sustain profitability in the future.

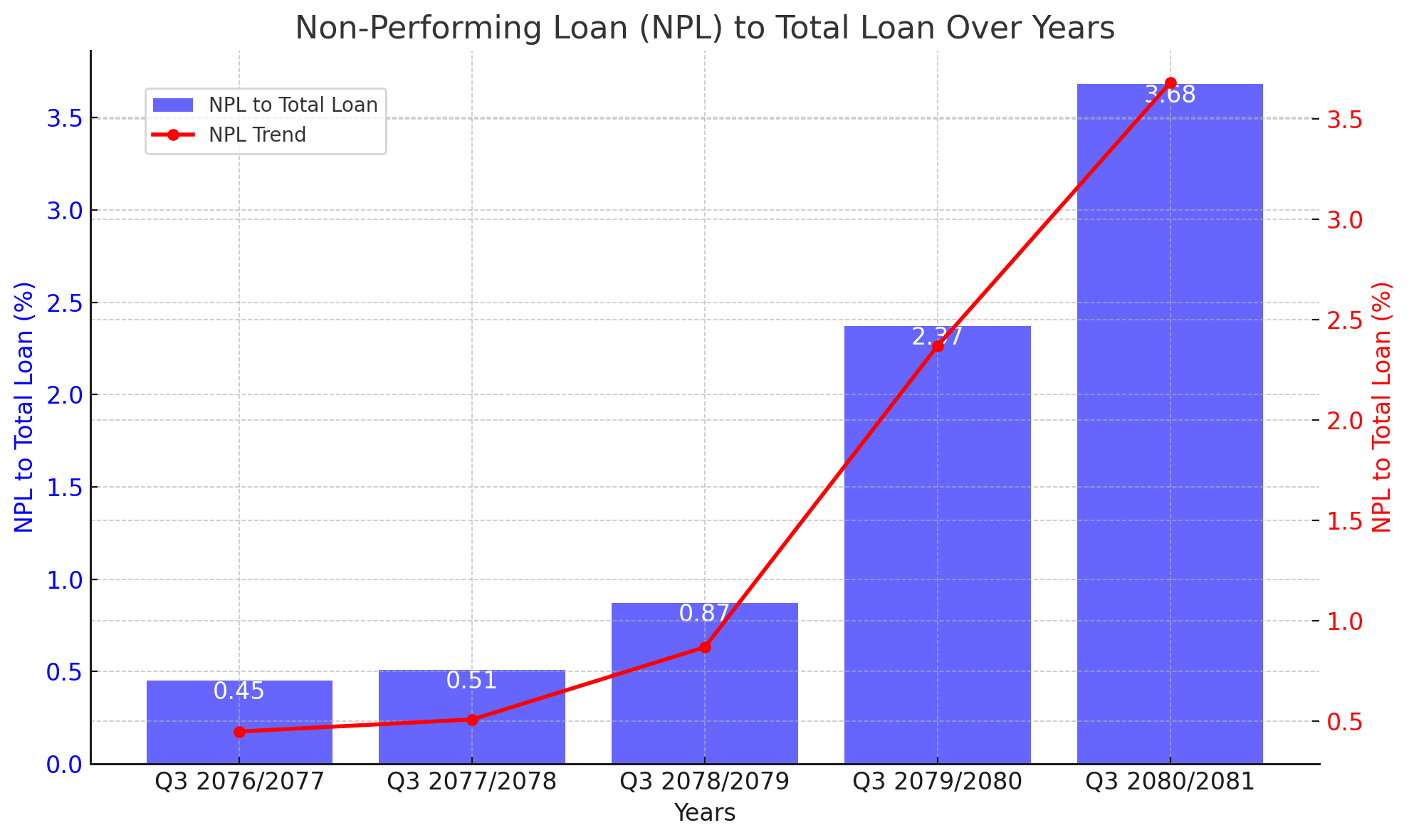

MBL's Non-Performing Loans Rise Dramatically in Q3 2080/2081

MBL has experienced a significant increase in its Non-Performing Loans (NPL) to Total Loan ratio in the third quarter of the fiscal year 2080/2081. This uptick raises concerns about the bank's loan portfolio quality and risk management practices.

Analysis of NPL Over Five Years

The NPL ratio for Q3 2080/2081 is reported at 3.68%, a notable rise from 2.37% in the previous year. This trend is even more alarming when compared to the NPL ratios of the past five years:

Q3 2076/2077: 0.45%

Q3 2077/2078: 0.51%

Q3 2078/2079: 0.87%

Q3 2079/2080: 2.37%

Q3 2080/2081: 3.68%

Interpretation of the Data

The steep increase from 0.87% in Q3 2078/2079 to 3.68% in Q3 2080/2081 signifies a troubling trend. This rise in NPL indicates that a growing portion of MBL's loans are not performing as expected, which could signal underlying issues in the bank's lending practices or the financial health of its borrowers.

Possible Factors Contributing to the Increase

Economic Downturn: An economic slowdown or recession can lead to higher default rates as borrowers struggle to meet their loan obligations.

Lending Practices: Aggressive lending without proper risk assessment might have contributed to the rise in non-performing loans.

Sectoral Challenges: Specific sectors that MBL has significant exposure to might be facing financial difficulties, impacting loan performance.

Regulatory Environment: Changes in regulatory frameworks or stricter enforcement of existing regulations could have affected loan classifications, leading to a higher reported NPL ratio.

Moving Forward

For MBL, it is imperative to conduct a thorough review of its lending practices and risk management policies. Strengthening credit assessment processes, diversifying the loan portfolio, and implementing effective monitoring systems will be crucial steps. Additionally, engaging with borrowers to understand their challenges and providing support where feasible can help mitigate further loan defaults.

Conclusion

The dramatic rise in MBL's Non-Performing Loan ratio in Q3 2080/2081 is a red flag that necessitates immediate attention. Addressing this issue with robust strategies will be vital for maintaining the bank's financial stability and investor confidence. The bank must adopt a proactive approach to manage and reduce its NPL ratio to ensure sustainable growth and profitability in the future.

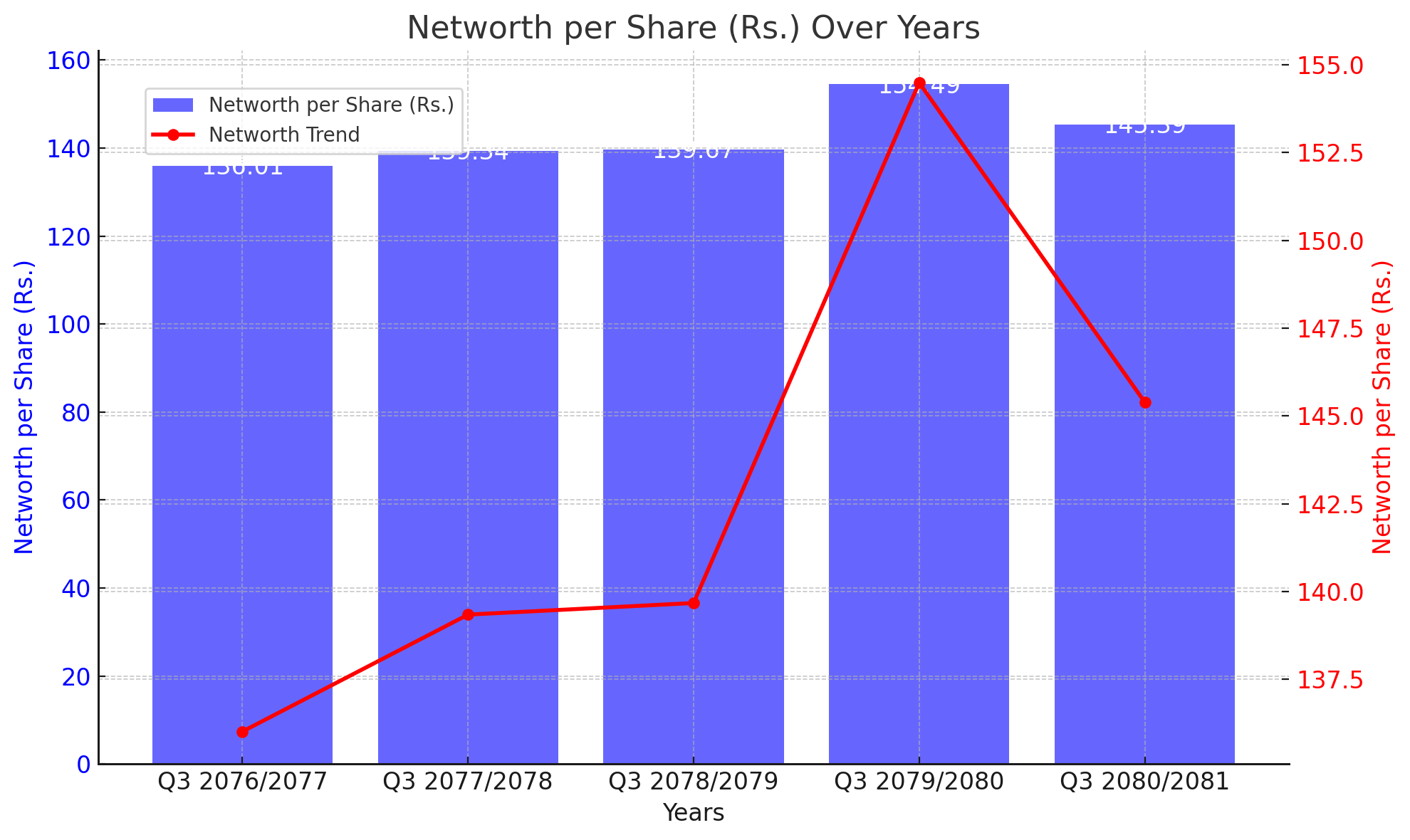

MBL's Networth per Share Shows Fluctuating Trends Over Five Years

MBL's Networth per Share (NPS) has exhibited noticeable fluctuations over the past five years, with a slight decline in the third quarter of the fiscal year 2080/2081 compared to the previous year. This data provides insight into the company's overall financial health and equity value on a per-share basis.

Analysis of Networth per Share Over Five Years

The NPS for Q3 2080/2081 stands at Rs. 145.39, down from Rs. 154.49 in the previous year. The trend over the past five years is as follows:

Q3 2076/2077: Rs. 136.01

Q3 2077/2078: Rs. 139.34

Q3 2078/2079: Rs. 139.67

Q3 2079/2080: Rs. 154.49

Q3 2080/2081: Rs. 145.39

Interpretation of the Data

The Networth per Share has generally shown a positive trend from Q3 2076/2077 to Q3 2079/2080, with a peak in Q3 2079/2080. However, the subsequent decline in Q3 2080/2081 raises some concerns about the recent financial performance and asset valuation of MBL.

Possible Factors Contributing to the Fluctuations

Asset Revaluation: Changes in the valuation of assets and liabilities can significantly impact the net worth per share. An increase in asset value or a reduction in liabilities can enhance NPS, and vice versa.

Equity Changes: Issuance or buyback of shares, along with changes in retained earnings, can affect the net worth per share. Higher retained earnings typically boost the NPS.

Market Conditions: Broader economic and market conditions influence the financial health of companies. Economic downturns or unfavorable market conditions might lead to lower asset values, impacting the NPS.

Operational Performance: The operational efficiency and profitability of MBL directly contribute to its net worth. Improved performance leads to higher retained earnings, positively affecting NPS.

Moving Forward

For MBL, the focus should be on stabilizing and enhancing its net worth per share. Strategies could include effective asset management, optimizing operational performance, and maintaining a healthy balance sheet. Transparent communication with shareholders about the reasons for the fluctuations and the steps being taken to address them is also crucial for maintaining investor confidence.

Conclusion

The fluctuating trend in MBL's Networth per Share over the past five years reflects the dynamic nature of its financial health and equity value. While there was a peak in Q3 2079/2080, the subsequent decline in Q3 2080/2081 suggests the need for strategic measures to sustain and enhance the net worth per share. By focusing on asset management, operational efficiency, and transparent communication, MBL can work towards a more stable and positive financial outlook in the coming years.

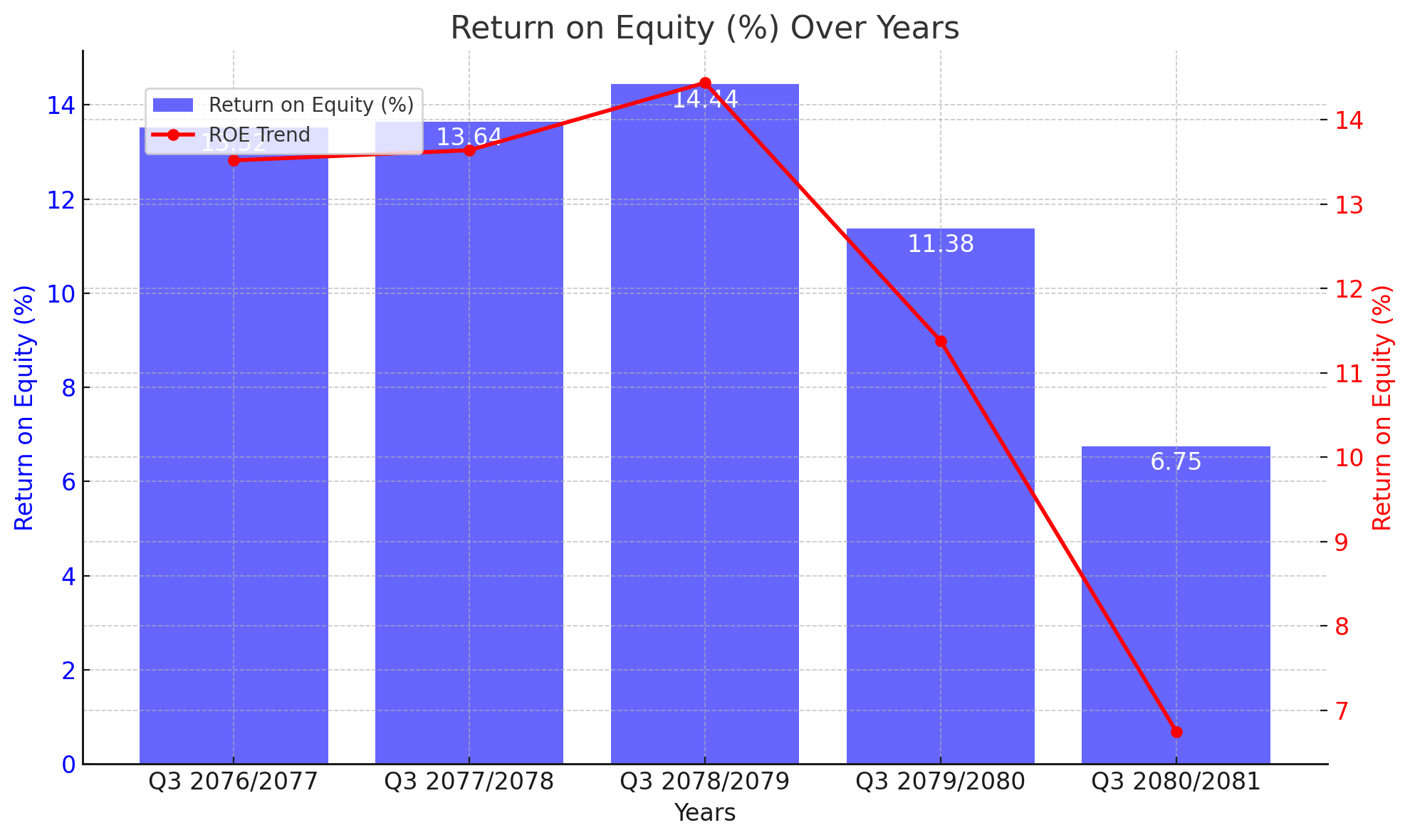

MBL's Return on Equity Experiences Sharp Decline in Q3 2080/2081

MBL has reported a significant decline in its Return on Equity (ROE) for the third quarter of the fiscal year 2080/2081. This decrease is a cause for concern, highlighting potential issues in the company's profitability and efficiency in generating returns from shareholders' equity.

Analysis of Return on Equity Over Five Years

The ROE for Q3 2080/2081 stands at 6.75%, a drastic drop from 11.38% in the previous year. Over the past five years, MBL's ROE has shown the following pattern:

Q3 2076/2077: 13.52%

Q3 2077/2078: 13.64%

Q3 2078/2079: 14.44%

Q3 2079/2080: 11.38%

Q3 2080/2081: 6.75%

Interpretation of the Data

The trend indicates a peak in ROE at 14.44% in Q3 2078/2079, followed by a steady decline over the subsequent years. The sharp decrease to 6.75% in Q3 2080/2081 suggests that MBL's ability to generate profit from its equity base has weakened considerably.

Possible Factors Contributing to the Decline

Decreased Profitability: A reduction in net income due to higher expenses, lower revenues, or both can directly impact ROE. Economic challenges or increased competition might have affected profitability.

Increased Equity Base: If the equity base has grown significantly without a corresponding increase in net income, the ROE will decline. This could happen due to new equity issuance or retained earnings that are not generating adequate returns.

Operational Inefficiencies: Inefficiencies in the company's operations, leading to higher costs and lower margins, can adversely affect net income and, consequently, ROE.

Market Conditions: Unfavorable market conditions and economic downturns can impact overall business performance, reducing profitability and returns on equity.

Moving Forward

To address the declining ROE, MBL needs to focus on improving its profitability and operational efficiency. Strategies may include optimizing cost structures, enhancing revenue streams, and improving asset utilization. Additionally, effective risk management and strategic investments can help bolster net income.

Conclusion

The significant decline in MBL's Return on Equity in Q3 2080/2081 underscores the need for immediate strategic interventions. By addressing the underlying factors contributing to reduced profitability and efficiency, MBL can work towards stabilizing and improving its ROE. Transparent communication with stakeholders about the challenges and the steps being taken to mitigate them will be crucial in maintaining investor confidence and driving long-term growth.

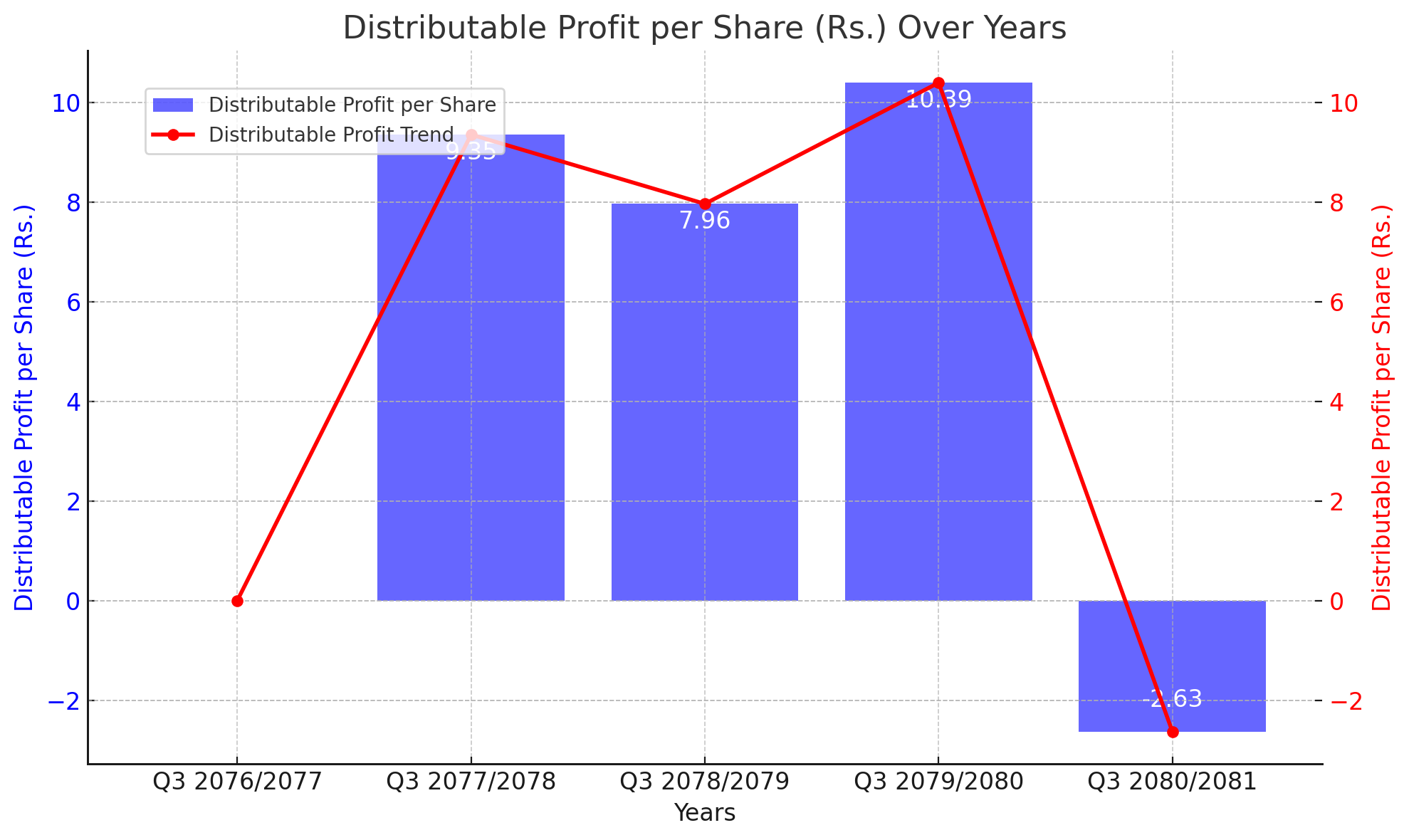

MBL Reports Negative Distributable Profit per Share in Q3 2080/2081

MBL has reported a negative Distributable Profit per Share (DPS) for the third quarter of the fiscal year 2080/2081. This significant downturn highlights potential financial challenges and poses concerns about the company's ability to distribute profits to its shareholders.

Analysis of Distributable Profit per Share Over Five Years

The DPS for Q3 2080/2081 stands at -Rs. 2.63, a drastic decline from Rs. 10.39 in the previous year. The trend over the past five years is as follows:

Q3 2076/2077: Rs. 0

Q3 2077/2078: Rs. 9.35

Q3 2078/2079: Rs. 7.96

Q3 2079/2080: Rs. 10.39

Q3 2080/2081: -Rs. 2.63

Interpretation of the Data

The Distributable Profit per Share has shown variability over the past five years, with significant positive values in Q3 2077/2078 through Q3 2079/2080. However, the sharp decline to a negative value in Q3 2080/2081 indicates a concerning shift in MBL's financial performance.

Possible Factors Contributing to the Decline

Decreased Net Income: A substantial reduction in net income, potentially due to increased expenses, decreased revenues, or both, can lead to a negative distributable profit.

Economic Conditions: Unfavorable economic conditions, including market volatility or a downturn, could adversely impact MBL's profitability and, consequently, its ability to generate distributable profits.

Operational Challenges: Internal operational inefficiencies or challenges may have contributed to higher costs and lower margins, affecting the overall profitability.

Exceptional Expenses: One-time or exceptional expenses, such as legal settlements or restructuring costs, could have significantly impacted the net income available for distribution.

Moving Forward

To address the negative DPS, MBL needs to focus on improving its operational efficiency and profitability. Strategies could include cost optimization, revenue enhancement, and effective risk management. Transparent communication with shareholders about the challenges and the measures being taken to mitigate them will be crucial for maintaining investor confidence.

Conclusion

The negative Distributable Profit per Share reported by MBL in Q3 2080/2081 underscores the need for immediate strategic interventions to stabilize and improve financial performance. By addressing the underlying factors contributing to the negative profit and implementing robust strategies, MBL can work towards restoring positive distributable profits and ensuring sustainable growth in the future.